[ad_1]

Photographer: Callaghan O’Hare / Bloomberg

Photographer: Callaghan O’Hare / Bloomberg

As OPEC + ministers virtually gather this week, the city that traditionally hosts their meetings will be on lockdown. Vienna’s Christmas markets will be closed, the famous Ringstrasse boulevard silent. For the oil ministers, the scene must call for caution.

But while the Austrian capital provides a dramatic example of how the the second wave of the pandemic closes the economies of Europe and the United States, the global picture is more nuanced.

In Asia, the situation is almost the opposite of that in Vienna. The streets in India were full during the recent celebration of Diwali; The Golden Week holiday in China saw millions of people take cars, trains and even planes to visit loved ones across the country.

Central Vienna on November 17. Vienna is currently closed.

Photographer: Helmut Fohringer / AFP / Getty Images

The east-west divide is an additional puzzle for OPEC +, which on November 30-December. You have to decide whether to delay an increase in production scheduled for January – and if so, for how long. And there is another crucial divide in the global oil market: While demand for gasoline and diesel has returned to about 90% of its normal level, jet fuel consumption is languishing at around 50%.

“The magnitude of the shock and the inequality of its impacts imply a recovery process that is far from fluid,” said Bassam Fattouh, director of the Oxford Institute for Energy Studies.

Delegates to the 177th OPEC meeting in Vienna in December 2019.

Photographer: Stefan Wermuth / Bloomberg

Privately, OPEC + delegates talk about the imbalance of the recovery, both geographically and between refined products. More and more, they talk about another segmentation: the quality of crude oil. The market for denser, more sulphurous crude, known as heavy-acid, is tight, mainly due to production cuts in Saudi Arabia, Russia and other large producers. But the so-called light sweet market is saturated, in part because Libyan barrels returned to the market after a cease-fireand European refiners are consuming less North Sea crude.

All of these factors make the deliberations of OPEC + ministers more difficult. And they only have one blunt tool at their disposal: increase or decrease overall production. OPEC + countries are not targeting gasoline or jet fuel production, only crude.

There is also a geographic handicap: most of their oil goes to Asia, where demand is high, rather than Europe and America, where it is weaker. That means there’s little they can do to address the glut where it matters. Even quality is an issue: OPEC mainly pumps heavy-sour crude and there is little that can be done to reduce the excess light-soft crude.

There is some consolation. While the recovery in oil demand that started in May stammered in October and November when the second wave took hold, it did not have the same impact on the market as it did at the start of the year. . The lockdowns in Europe are not as bad as the first wave, and demand in Asia is increasing – not just in China, but also in India, Japan and South Korea.

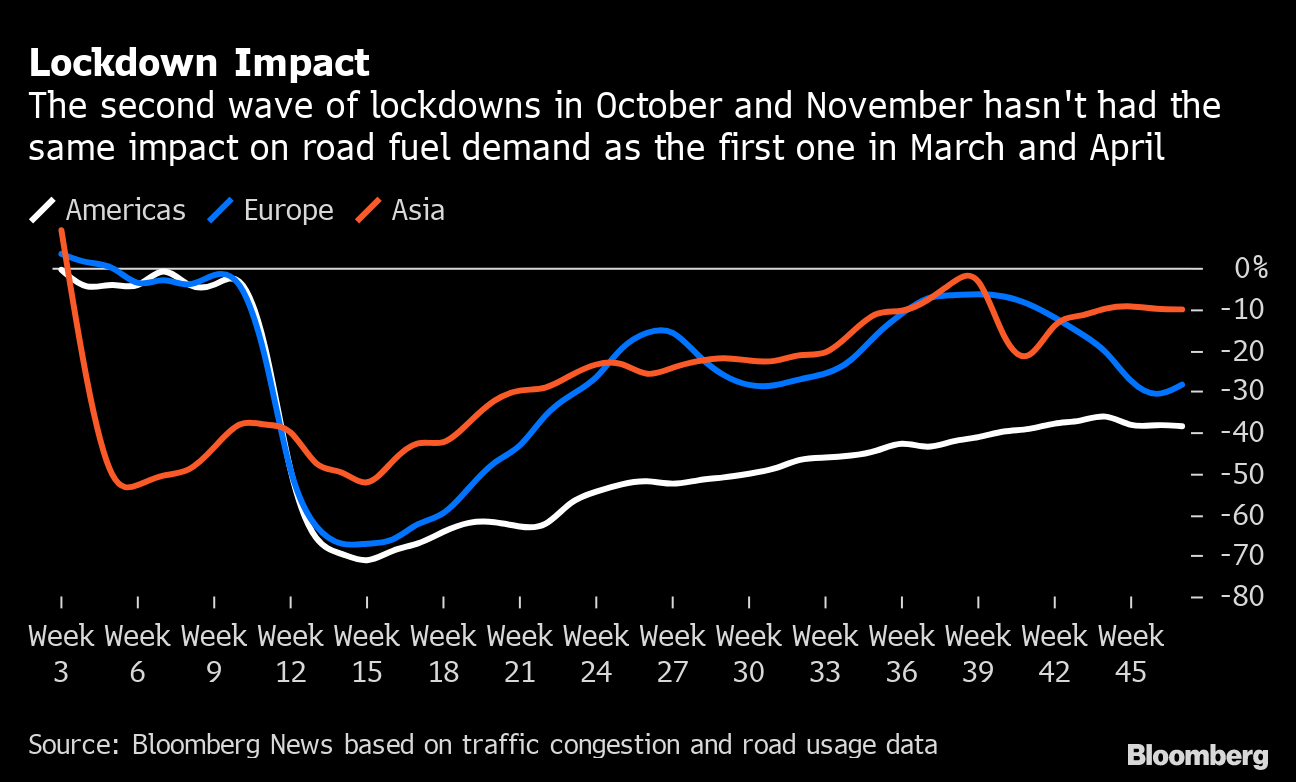

Lockdown impact

The second wave of closures in October and November did not have the same impact on road fuel demand as the first in March and April

Source: Bloomberg News based on data on traffic congestion and road use

High-frequency road use data shows a drop in early November of around 30% from pre-Covid levels, down from nearly 70% in late March and early April, according to an index compiled by Bloomberg News. The most recent data suggests that demand for on-road fuel hit a low around November 15 and has been picking up since. With European nations facilitating lockdowns in the raceUntil At Christmas, demand is expected to pick up again.

Taken together, this all means that the market is not as bad as it was a few weeks ago. Oil prices reflect the more positive tone: Brent rallied well above $ 45 a barrel, and the shape of the the curve reversed, with close contracts trading at a premium over subsequent contracts. This dynamic, known as a downshift and traditionally a bullish signal, means that demand exceeds supply.

The physical market, where actual barrels change hands, is also showing signs of strength: Chinese refiners’ favorite crude varieties are rising in premium. Take ESPO crude from Russia, a quality that independent Chinese refiners known as teapots like to buy. In the most recent tenders, it changed hands to $ 2.85 a barrel above its benchmark, down from 55 cents in mid-October.

Beyond the next quarter, the outlook improves further.

Many are already optimistic about the impact of vaccines against the virus on oil demand. If they’re right, by the middle of this year when OPEC is likely to reconvene, the streets of Vienna will once again be full of tourists, often bewildered to see oil ministers followed by packages. of television cameras across the Austrian capital. The cartel tentatively plans to hold its biannual International Petroleum Seminar, a two-day industry festival, at the Hofburg Imperial Palace in June 2021.

“The effectiveness and availability of vaccines indicate a sufficiently large recovery in oil demand next year to allow OPEC to achieve both a rebalancing of excess stocks and significantly increase production,” said Damien Courvalin, Oil Analyst at Goldman Sachs Group Inc.

To delay or not to delay

If OPEC + continues its production increase in January, world oil stocks will increase in Q1 2021. But a 3-month delay eliminates the build-up of stocks

Source: OPEC internal analysis

For now, however, OPEC + still has work to do. If the cartel is to continue to drain inventory accumulated earlier this year, it must keep the market in deficit, rather than simply balancing supply and demand. With Libyan production rebounds, OPEC economists estimate global stocks would increase by around 200,000 barrels per day during the first quarter 2021 if the group increases its production as planned in January. If that delayed the three-month hike, inventories would instead drain by around 1.7 million barrels per day between January and March, an amount similar to what he expects in the fourth quarter of 2020.

“The job is far from done,” said Gordon Gray, global head of oil and gas equity research at HSBC Holdings Plc.

[ad_2]

Source link