/cloudfront-us-east-2.images.arcpublishing.com/reuters/N3PPWCE525M5HHT2CKIQNJ47O4.jpg)

[ad_1]

LONDON, Oct. 4 (Reuters) – Demand for coal and natural gas has surpassed pre-COVID-19 highs, with oil not far behind, pushing back hopes the pandemic would accelerate the transition to energy clean from fossil fuels.

Global natural gas shortages, record gas and coal prices, an electricity crisis in China and a three-year record high in oil prices tell a story: demand for energy has exploded and the world has exploded. still need fossil fuels to meet most of these energy needs. .

“The drop in demand during the pandemic was entirely linked to governments’ decision to restrict movement and had nothing to do with the energy transition,” Cuneyt Kazokoglu, head of demand analysis at Reuters, told Reuters. petroleum at FGE.

“The energy transition and decarbonisation are strategies that last a decade and do not happen overnight. “

More than three-quarters of global energy demand is still met by fossil fuels and less than a fifth by non-nuclear renewables, according to the energy watchdog, the International Energy Agency.

Energy transition policies are criticized for soaring energy prices. In some places they are having an impact, such as in Europe where high carbon prices aimed at reducing emissions have made utilities reluctant to fire up coal plants to make up for the shortage.

In China, emission reduction policies have contributed to the government’s decision to ration energy to heavy industry.

But much of the rise in energy prices is simply due to the fact that producers took huge amounts of capacity offline last year when the pandemic caused an unprecedented drop in demand.

Several factors mean that temporary shortages may not last.

They could ease with an OPEC decision to open the taps to release the supply it held back in the first COVID assault, likely new liquid natural gas (LNG) production to come after a drop prices over the past decade and a decline by the Chinese government on pricing that has undermined coal-fired power generation.

RENEWABLES A “SOLUTION, NOT A CAUSE”

Producers of gas, coal and, to a lesser extent, oil have been caught off guard by the economic recovery, largely triggered by government stimulus spending in energy-intensive industries.

National policies have also played a role in the problems of electricity supply. In China, state-imposed electricity prices mean utilities simply cannot afford to burn coal and sell electricity because the cost of coal is too high to make a profit.

Chinese utilities are producing below capacity to avoid losing money, not because they cannot produce more.

Meanwhile, most gas projects take several years to design and build, so the scarcity now reflects investment decisions made before the pandemic – and before the energy transition gained political momentum.

The head of the Paris-based IEA said energy transition policies were not to blame for the crisis.

“Well-managed clean energy transitions are a solution to the problems we see in the gas and electricity markets today – not the cause of them,” Fatih Birol said in a statement.

2020 LOSSES CLEARED

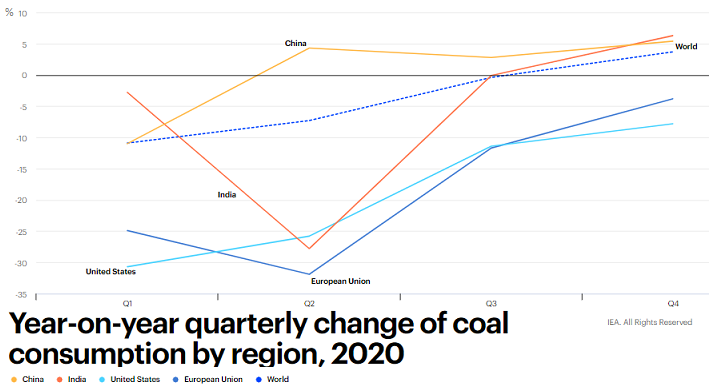

Yet IEA data shows global demand for coal, the largest source of CO2 emissions, has exceeded pre-pandemic levels late last year.

Global coal supplies are tight because China, responsible for about half of global production, tightened mine safety rules after a series of accidents, undermining the supply.

This left China to import more coal from Indonesia, in turn leaving less for other importers such as India.

Global demand for coal is expected to grow 4.5% this year, exceeding 2019 levels.

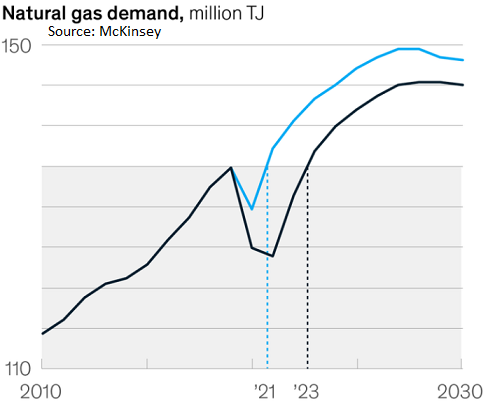

Global demand for natural gas fell 1.9% last year, a smaller drop than for other energy sources, as utilities increased electricity production to meet winter heating needs.

But the IEA predicts that gas demand will rise 3.2% in 2021 to over 4 trillion cubic meters, wiping out 2020 losses and pushing demand above 2019 levels.

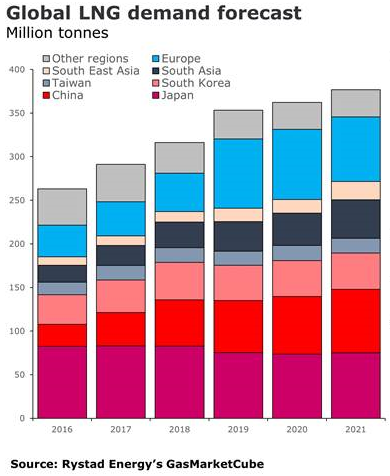

The cold in the northern hemisphere, said Rystad Energy, an Oslo-based consultancy firm, “has caused an increase in demand for coal, liquefied natural gas (LNG), electricity and even some oil ( who) is here to stay “.

LNG accounts for just over 10% of global supply, but it is more easily marketed globally and therefore can be deployed more easily to cover short-term supply shortages.

“The impressive price spikes and their gap between summer and winter will widen, especially for gas, both natural and liquefied,” Rystad added, as prices are higher in winter than in summer.

TENDER GAPS, SHORT-TERM RALLIES

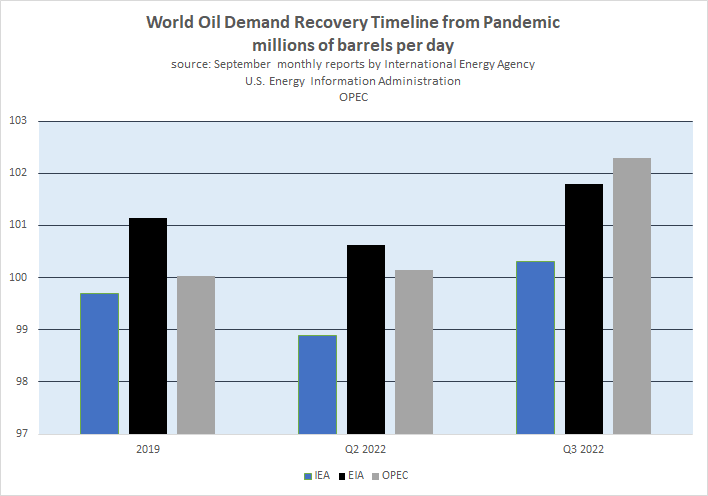

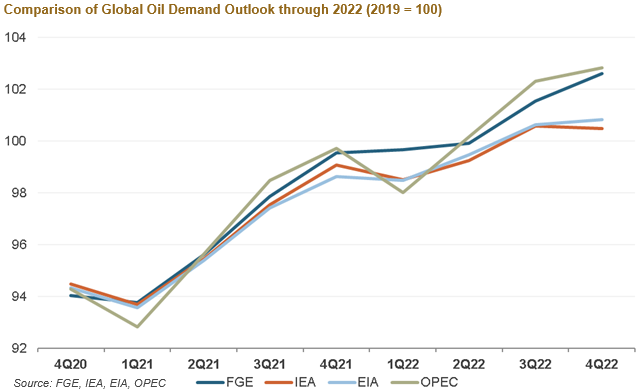

Last to catch up, demand for oil is expected to rebound to pre-pandemic levels above 100 million barrels a day next year, according to four of the major monitoring groups.

The high prices in the oil markets are due to the fact that OPEC and allied producers still have millions of barrels per day of oil production offline after making record cuts in supply during the pandemic to respond to the falling demand for transportation fuel.

The OPEC producer club offers the most robust forecast for a rebound in demand, placing the recovery date in the second quarter of 2022.

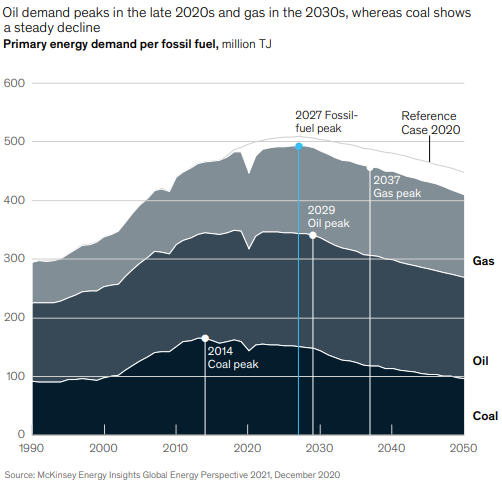

In the more distant future, with most forecasters predicting a peak in demand for fossil fuels over the next two decades and the IEA advising against new projects to ensure net zero emissions, larger supply gaps could fuel more. price shocks.

“Fossil fuel prices will remain volatile,” said Nikos Tsafos, senior researcher at the Center for Strategic and International Studies (CSIS).

“The risk of a supply-demand imbalance is greater in a shrinking market where the case for further investment is weak, which could produce short-term rallies.”

Writing by Noah Browning; edited by David Evans and Ed Osmond

Our Standards: The Thomson Reuters Trust Principles.

[ad_2]

Source link