[ad_1]

it is rare to see Alibaba Group Holding Limited (NYSE: BABA) the price / earnings (or “P / E”) ratio of 19.1x is as close as the median US market P / E of 18x. Moreover, the company itself continues to grow, and the company still occupies a dominant position among the Chinese competitors. However, as we all know, the main risk lies in the government’s approach to the company, and today we will take a look at the risks of investing in a Chinese company and what the current P / E means for Alibaba. .

View our comprehensive fundamental analysis for Alibaba Group Holding

The risks of investing in Chinese stocks

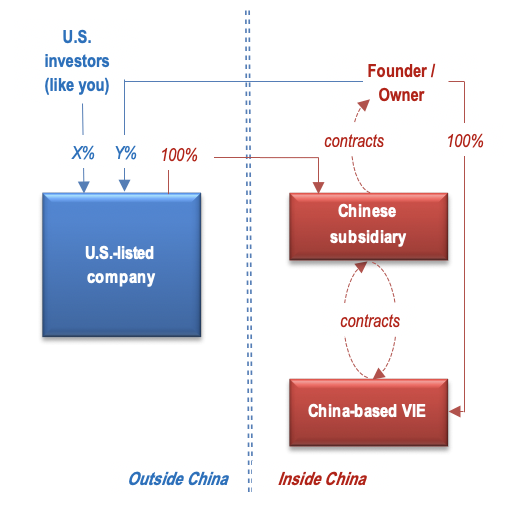

The most important thing to note is that investors are not Alibaba shareholders. They are in fact shareholders of the Cayman Islands Shell Company which represents Alibaba (this is called a variable interest entity – VIE). It is this company that is listed on the NYSE, and has a contract with the Chinese entity to represent their operations.

The SEC explains this structure in detail, and a high-level plan can be represented with this graphic:

What we can see is that as investors in Chinese equities we have several degrees of separation. The reason is that the Chinese government has loose regulations preventing US investors from owning shares in Chinese companies. And as these companies grew, actually subsidized by US and international investors, the government has been passive, but in recent months has launched a campaign that began with a crackdown on tech companies.

The worst-case scenario that could happen is that the government announces to companies that they are (and indeed are) in violation of the law, and will be penalized for doing so by forcing them to sever ties with American investors. .

Every Chinese equity investment thesis carries with it the assumption that this is not happening.

A great prize for the winnings

Assuming this big IF doesn’t happen, we’re going to take a look at how expensive or cheap Alibaba is for investors.

Alibaba has a P / E close to the median of the US market, but the company is in the technology sector, and the P / E 26.7x is much more representative of the pricing of similar companies in this industry.

The P / E of 19.1x is the lowest since 2016.

It is very likely that on a pure P / E ratio basis the company is currently a good deal.

Eager to know how analysts think Alibaba Group Holding’s future compares to the industry? In this case, our free report is a great place to start.

Growth of Alibaba Group Holding

There is an inherent assumption that a company should match the market for P / E ratios like Alibaba Group Holding to be considered reasonable.

Looking back at the results of the past year, discouragedly, the company’s profits have fallen by around 18%.

Yet the the last three-year period saw an excellent overall increase of 141% in EPS, despite its unsatisfactory short-term performance. While it’s been a bumpy ride, it’s still fair to say that earnings growth recently has been more than enough for the company.

Looking to the future now EPS is expected to grow 5.3% per year over the next three years, according to analysts who follow the company.

With this information, we find it interesting that Alibaba Group Holding is trading at a P / E quite similar to the market.

Key points to remember

As we have seen, investing in VIE’s links with Chinese companies involves a different kind of risk. If this risk is acceptable to investors, it is likely that Alibaba is currently trading cheaply as a stock.

In addition, the stock is expected to continue to grow both revenue and profit, making it a growth stock with a lower value. It’s rare, but the additional risk factor deserves caution.

As a general rule, we prefer to limit the use of the price / earnings ratio to establishing what the market thinks about the overall health of a business.

And what about other risks? Every business has them, and we’ve spotted 2 warning signs for Alibaba Group Holding you should know.

Simply Wall St analyst Goran Damchevski and Simply Wall St have no positions in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts using only unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell shares and does not take into account your goals or your financial situation. Our aim is to bring you long-term, targeted analysis based on fundamental data. Note that our analysis may not take into account the latest announcements from price sensitive companies or qualitative documents.

Do you have any feedback on this item? Are you worried about the content? Contact us directly. You can also send an email to [email protected]

[ad_2]

Source link