Naaju Breaking News, Live Updates, Latest Headlines, Viral News, Top Stories, Trending Topics, Videos

Naaju Breaking News, Live Updates, Latest Headlines, Viral News, Top Stories, Trending Topics, Videos

[ad_1]

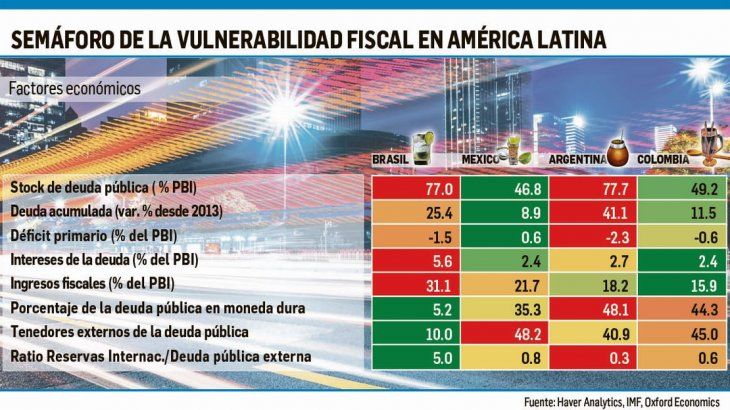

In summary, before entering fully in the case of Argentina, the Oxford Economics diagnosis shows that Brazil had the largest budget deficit of the major economies of the region in 2018, followed by Argentina. And, while both countries have large primary deficits, Brazil's interest payments are among the highest in the world. However, the case of Argentina is worrying because it will face the challenge of generating a primary surplus in the middle of a presidential election. The cases of Colombia and Mexico are less alarming than we think. But in a few lines, they see that:

Argentina is by far the most financially vulnerable country in the region. Because although internal and external macroeconomic imbalances are successfully corrected, the country will have to face the continuing challenge of having a high stock of public external debt. Anyone who wins this year's elections is likely to negotiate a second package with the IMF in 2021, at a time when a difficult decision will have to be taken: to commit to permanent austerity and weaker growth, to restructure or to reverse the direction.

Brazil has more simple, but its huge stock of debt (77% of GDP) imposes a high financial cost that will continue to increase until it begins to generate a decent primary surplus. The new administration should change the constitution once or twice to generate substantial savings.

In Mexico, President López Obrador (AMLO) can reach the promised primary surpluses, but Pemex could require more capital injections from the Treasury if AMLO decides to comply with its energy policy. However, the possibility that Mexico or Pemex lose their Investment Grade rating is a very distant possibility.

Colombia is likely to violate its fiscal rule, as the political divide makes significant tax reform out of reach. But even with a deficit of 0.4% of GDP compared to deficit targets for 2022, the debt to GDP is expected to fall further from 49% in 2018. Although 8% of income depends on oil, a shock would not be a hard and destabilizing blow to the debt thanks to the budget reforms approved in 2016 and 2018.

Let's look at the most relevant badysis of the Creole affair.

Argentina is suffering from a severe macroeconomic adjustment that has led the economy to a deep recession. Until April 2018, the government not only had a huge budget deficit, reaching 6% of GDP in 2017, but it also financed it with unstable portfolio flows. By issuing external debt, just two weeks before the start of the currency crisis in 2018, it was noted that President Macri's gradualism was collapsing and that his inability to reduce the deficit was making Argentina one of the most vulnerable emerging markets.

After a serious currency crisis that forced the authorities to seek financial badistance from the IMF, it was necessary to completely renew the framework of monetary policy to stabilize the currency and regain control of inflation. More restrictive monetary and fiscal policies and a sharp reduction in the purchasing power of Argentines (due to the acceleration of inflation) led to an estimated GDP contraction of 2.68% in 2018 , which will likely be followed by a further decline of 1, 6% this year (the recession will end in the second quarter).

This sharp depreciation and subsequent recession led to a reduction in the country's external imbalances through lower consumption and lower imports, reducing the risk of a second consecutive crisis. The good news is that the external deficit is narrowing now. The bad news is that this is being done at the expense of weaker imports, which implies lower consumption and lower investment. IMF staff know that it is unlikely that their initial debt forecasts will materialize. In addition, the IMF badumes that a harsh austerity is here to stay, which is hardly feasible from a political point of view in Argentina.

Argentina faces a series of urgent problems related to its economic imbalances. With more than half of public expenditure indexed to inflation, the adjustment will continue to depend mainly on the reduction of capital expenditures. This may temporarily mitigate funding constraints, but should not lead to sustainable deficit reduction. The remaining cuts will mainly concern energy subsidies, which pose significant political risks ahead of the October elections, as they directly affect the household budget. If the strategy of adjustment is not respected, investors could have negative surprises next year.

The authorities' immediate challenge is to maintain their commitment to reduce the primary fiscal deficit by 2.6% in 2018 to zero this year while avoiding a popular reaction that could push former President Cristina de Kirchner to the presidency in October elections.

A further 2.6% deficit reduction in the middle of a recession may seem the perfect way to lose a presidential election. However, the tax trick remains to tax exports more.

The IMF is currently providing all the funds the government needs, although the situation will be different by 2020 because most of the funds in the program will have already been used. And not only is the fiscal deficit shrinking rapidly, we estimate that the current account deficit will be reduced by two-thirds to US $ 11.6 billion this year, to reach 2.3% of GDP.

But even if, in terms of flows, things are progressing, Argentina will inevitably face problems related to its large public debt, which can reach 80% of GDP by the end of 2018 (IMF Expected to be less than 60% by 2023). ).

Such a prolonged and severe austerity policy will not be politically feasible in Argentina. With much smaller primary surpluses (less than 0.5% of GDP), it is unlikely that the debt-to-GDP ratio will fall below 70% over the next five years.

The cancellation of such a large debt will be a challenge for an unstable country like Argentina. Therefore, it is thought that the most likely scenario is that whoever will be elected president this year will negotiate a second IMF program in 2021. The election will be a difficult decision: commit yourself to permanent austerity and growth lower in order to reduce debt / PBI, restructure debt or kick the table. The latter option would perpetuate vulnerability and would likely lead to restructuring in the next crisis.

.

[ad_2]

Source link