[ad_1]

In 2013, I called Goldman Sachs a "snake oil salesman" for a $ 1 billion share buyback offer. Investors have since lost 91%. There are also tons of bonds, including a 100-year bond.

J.C. Penney, who has taken a step closer to what will ultimately be a bankruptcy filing and likely liquidation of the company, can be summarized as follows:

- 860 stores, compared to 1,100 in 2011;

- 95,000 employees

- A $ 4 billion debt, some of which will expire later this year and others over the next few years;

- $ 12 billion in annual sales down from $ 17 billion in 2011;

- $ 5 billion of net losses accumulated since 2011.

Sources told Reuters that the company had hired restructuring consultants. The hiring of restructuring advisers always makes sense: if the company can not force its creditors to reach an agreement on a debt restructuring that will probably cost them dearly, it will file bankruptcy. It is this threat of bankruptcy that weighs on the creditors that might incite them to accept losses resulting from negotiations rather than letting a bankruptcy court decide their fate.

But even after a debt restructuring, a zombie like J.C. Penney will probably fail a year or two later. Retailers are notoriously difficult to restructure. Most of them end up being liquidated. When a brand as famous as JC Penney fails, it is not because of an error, but because of years, even decades, of mismanagement and inability to s & d. Adapt to a changing environment – and thus to kill the brand.

At the news today, the actions of J.C. Penney [JCP] fell 17% from almost nothing to even less, now at $ 0.90.

What is surprising is not that it happens. E-commerce has completely crushed department stores. The chains, including the big brands Sears and Kmart, as well as Bon Ton stores, which have not made the transition, have already been dismembered as part of the brick and mortar merger.

But I am impressed by the length of zombie companies such as J.C. Penney who continue to feed on new sources of money by investors who believe in Wall Street's hype before being scammed.

So here is the example of J.C. Penney of how Wall Street entities, in this case Goldman Sachs, have conspired with the company to scam investors. In 2013, while I was still relatively new to my financial website and I was still using angry but technically correct terms that I might not use today with more kindness and gentleness, I wrote an article entitled "JC Penney and Goldman: Lies, Scams and Scams "- which started like this:

Why would anyone buy this shit? No, not the clothes in J.C. Penney's stores – that hardly anyone buys – but the stock he just sold.

Tsk, tsk, tsk, wash your mouth with soap, Wolf … And then this:

He hired Goldman Sachs as an underwriter – snake oil salesman This term would be more appropriate. He proposed to sell 84 million shares at $ 9.65 per share and granted Goldman a 30-day option to acquire up to 12.6 million more shares, for a total of 96.6 millions of shares. The agreement would raise up to $ 932 million.

The offer of shares has been planned in the utmost secrecy. And the day before the announcement of the sale of shares, and in order to inflate the course of action, CEO Myron E. Ullman III, fully involved in the sale of shares the next day, said that & # 39; He did not foresee a situation this year where "we would need to raise cash".

Lie lie. That's what keeps the zombies funded.

Yup, in September 2013, JC Penney, with the help of Goldman Sachs, who had been richly paid for it, was able to extract nearly $ 1 billion in new investors through to an offer of shares at $ 9.65 the action. This money from new investors saved former investors and kept the zombie alive, allowing it to refinance debt maturing in subsequent years and to lose the $ 5 billion balance mentioned above.

But the investors who bought these shares during the unfounded stock offer in September 2013 did not have to wait that long before they were cleaned up. Their investment is down 91%.

We are now nearing the end. Another sale of shares is out of the question. Refinancing of maturing debt is also likely. Everyone knows it's the turn of the creditors to lose money, whether in the bankruptcy court or outside.

Moody's evaluates J.C. Penney Caa3, just above the default (my aide-memoire in English on credit rating companies by S & P, Moody's and Fitch). The news of the debt restructuring will probably silence Moody's ears. A debt restructuring, even outside the bankruptcy court, is usually considered an event of default.

J.C. Penney has discussions with restructuring specialists – lawyers and business bankers – for several weeks, "some of these sources" told Reuters. One source said the restructuring talks are at an early stage. The goal is to find ways to restructure debt and obtain new funds to bail out former investors. This would keep the zombie alive a little longer. The creditors will be motivated by the threat of a bankruptcy filing hanging over their heads and they will have the choice.

With respect to the bonds that are part of the $ 4 billion long-term debt of J.C. Penney, there is a multitude of things, including wild things.

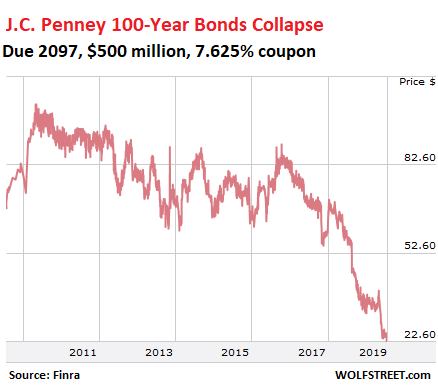

For example, in 1997, J.C. Penney was able to sell $ 500 million of 100-year unsecured bonds for a coupon of 7.625%. These data have collapsed and are now trading at 22.5 cents per dollar, according to Finra data. This means that investors believe that the company's chances of exceeding 2021 are virtually nil. The yield is 33% at the price of the day, and if you buy at that price, and if the company manages to pay interest over the year, these links would be a lot. If no, well …

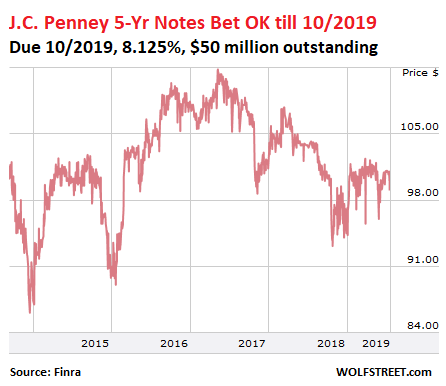

Then, the company issued $ 400 million five-year notes, issued in 2014. Of this amount, only $ 50 million is still outstanding and their maturity is October 1, 2019. Investors are certain that the company will be able to make sure that far and pay the bill with the money that he has on hand. It is currently trading at 99 cents a dollar:

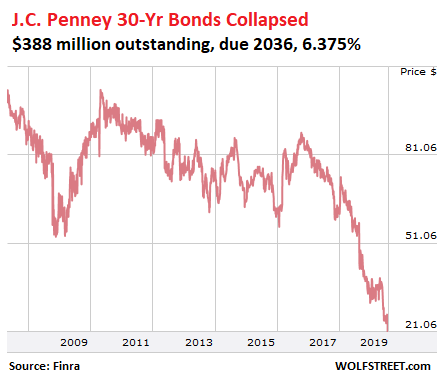

In 2007, J.C. Penney sold $ 700 million of unsecured bonds at age 30, with a coupon of 6.375%. Of these bonds, $ 388 million is still outstanding. They collapsed and are now trading at 21 cents a dollar, giving them a return of 31%. Investors who buy today calculate to receive only one additional year of interest payments, then after me the flood:

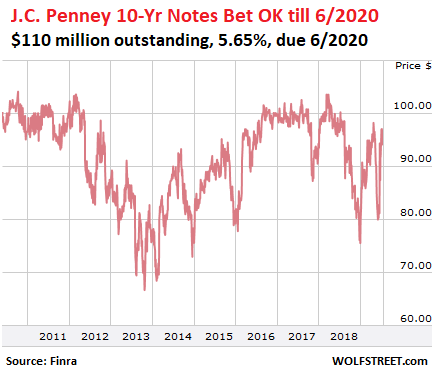

In 2010, the company sold $ 400 million worth of 10-year unsecured bonds with a 5.65% coupon. Of this amount, $ 110 million is still outstanding and their deadline is next June. These bonds experienced extreme fluctuations last year and this year, as investors badessed the chances that the company would succeed until June 2020. They are currently trading at around 93 cents a dollar, which indicates that they are pretty much certain, but not certain, these bonds will be repaid at face value on the due date, but a month ago they were less safe and bonds are trading at 80 cents on dollar:

Equity investors have been virtually eliminated and the remaining market value of $ 280 million will also be absorbed. Bond investors give the company a very limited life – hopefully, maybe a few years. This could be 2020 or 2021 in the best of scenarios, during which time the company will continue to consume money from investors.

But it was clear in 2013, when I wrote the article, and we are now at six, and it is still moving in the same direction towards the inevitable, and that it is much close to the inevitable, at hand really, and investors have lost a lot of money, and yet, they still plan to feed the zombie with new money to keep it lame a little longer.

Do you like to read WOLF STREET and want to support it? Using ad blockers – I fully understand why – but you want to support the site? You can give "beer money". I like it a lot. Click on the beer mug to find out how:

Would you like to be informed by email of the publication of a new article by WOLF STREET? Register here.

Source link