/cloudfront-us-east-2.images.arcpublishing.com/reuters/XFDXNT7Z75MLPA5BXJWQ46ULLM.jpg)

[ad_1]

The photo shows the headquarters of the Evergrande Automotive R&D Institute of the China Evergrande group in Shanghai, China on September 24, 2021. REUTERS / Aly Song

NEW YORK, Sept. 24 (Reuters) – Concerns over debt-strapped real estate developer China Evergrande (3333.HK) have warned investors of evidence the crisis could spill over into wider markets.

Evergrande, once China’s best-selling real estate developer, owes $ 305 billion, is cash-strapped, and investors fear a collapse poses systemic risks to China’s financial system and spill over into the world. Read more

So far, there have been few signs of strain in the money and credit markets, as well as in other areas, that would indicate the crisis was spreading beyond China.

“Evergrande’s debt link to other global financial players is modest, despite its size,” said Stan Shipley, fixed income strategist at Evercore ISI in New York.

“As a result, the risk of contagion is low. China has sufficient financial resources to cushion a possible bankruptcy or restructuring,” he added.

The situation remains tense, however, and few investors have forgotten the explosions in the money market during the global financial crisis of 2008, the sovereign disorder of the euro area of 2011 which effectively excluded European banks from interbank lending and, more recently, the coronavirus pandemic that rocked the global economy and led to massive bailouts from central banks.

Here are some key barometers of market stress that investors are observing:

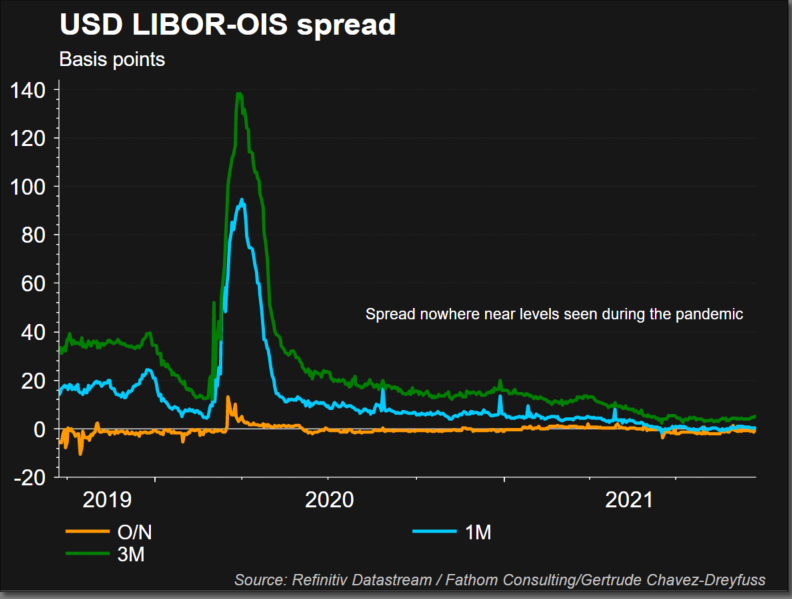

US LIBOR-OIS

The US LIBOR-OIS spread measures the difference between secured and unsecured loans in the US and is considered a measure of stress in money markets.

A higher spread suggests that banks are getting more nervous about lending to each other because the cost has gone up.

The LIBOR-OIS spread narrowed significantly to 3.2 basis points from a pandemic peak of 135.213 basis points in April last year on Friday, amid rising vaccinations and reopening of the American states.

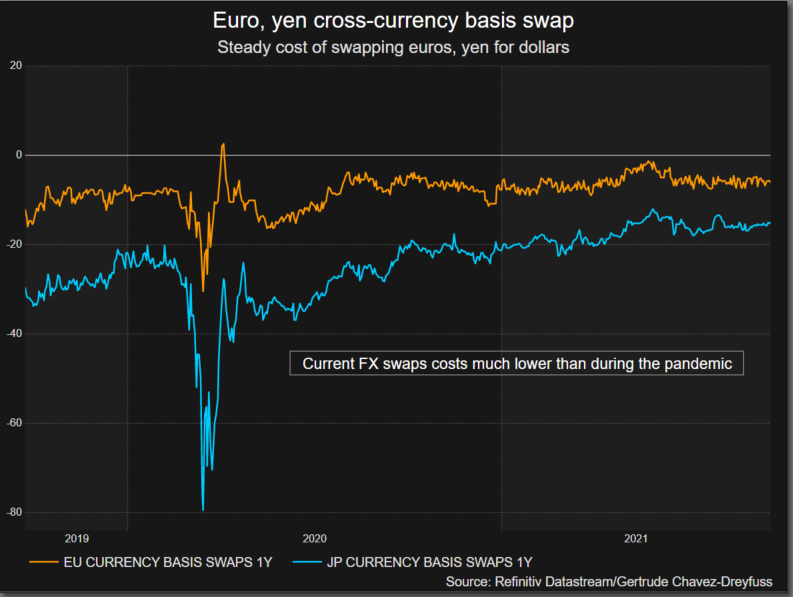

FX EXCHANGES

Currency swaps allow investors to raise funds in a particular currency from other funding currencies. For example, an institution with dollar funding needs can raise euros in the Euro funding markets and convert the proceeds into dollar funding obligations through a foreign exchange swap.

These instruments gained attention during the 2008 financial crisis and the eurozone debt crunch when global regulators poured billions of dollars to unfreeze the market.

One-year euro / dollar basis swaps, which measure European borrowers’ demand for dollars, were -11 basis points on Friday, signaling willingness to pay a bit more to get their hands on dollars.

In other words, investors have to pay around 11 basis points on interbank rates to swap one-year euros for dollars. As the most liquid currency in the world, the dollar is a popular destination for investors in uncertain times.

These levels are far from the highs observed during the pandemic or during the 2008 crisis.

The same goes for dollar / yen basis swaps, currently at -19.75 basis points on Friday, far from the -144 basis points reached in March 2020.

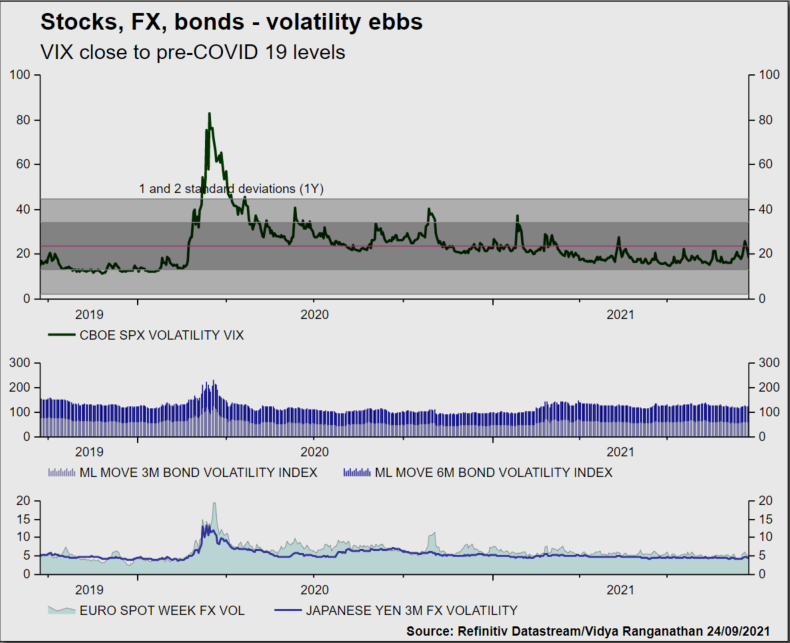

VOLATILITY OF BONDS, FX, SHARES

The volatility of the three asset classes – stocks, bonds, currencies – remained relatively moderate.

The Cboe Volatility Index (.VIX), which measures the implied volatility of the S&P 500 and is known as the “Wall Street fear gauge,” was at 20.38 on Friday, from a high of 85.47 in March. 2020.

The broader currency market volatility, as assessed by Deutsche Bank’s volume measure (.DBCVIX), was also on a downtrend. Late Thursday, the index was at 6.02, down significantly from the 14.17 affected during the pandemic.

The ICE BofA MOVE Index (.MOVE), which tracks traders’ expectations for fluctuations in the Treasury market, stood at 56.79 on Friday, up from 163.70 hit in mid-March last year.

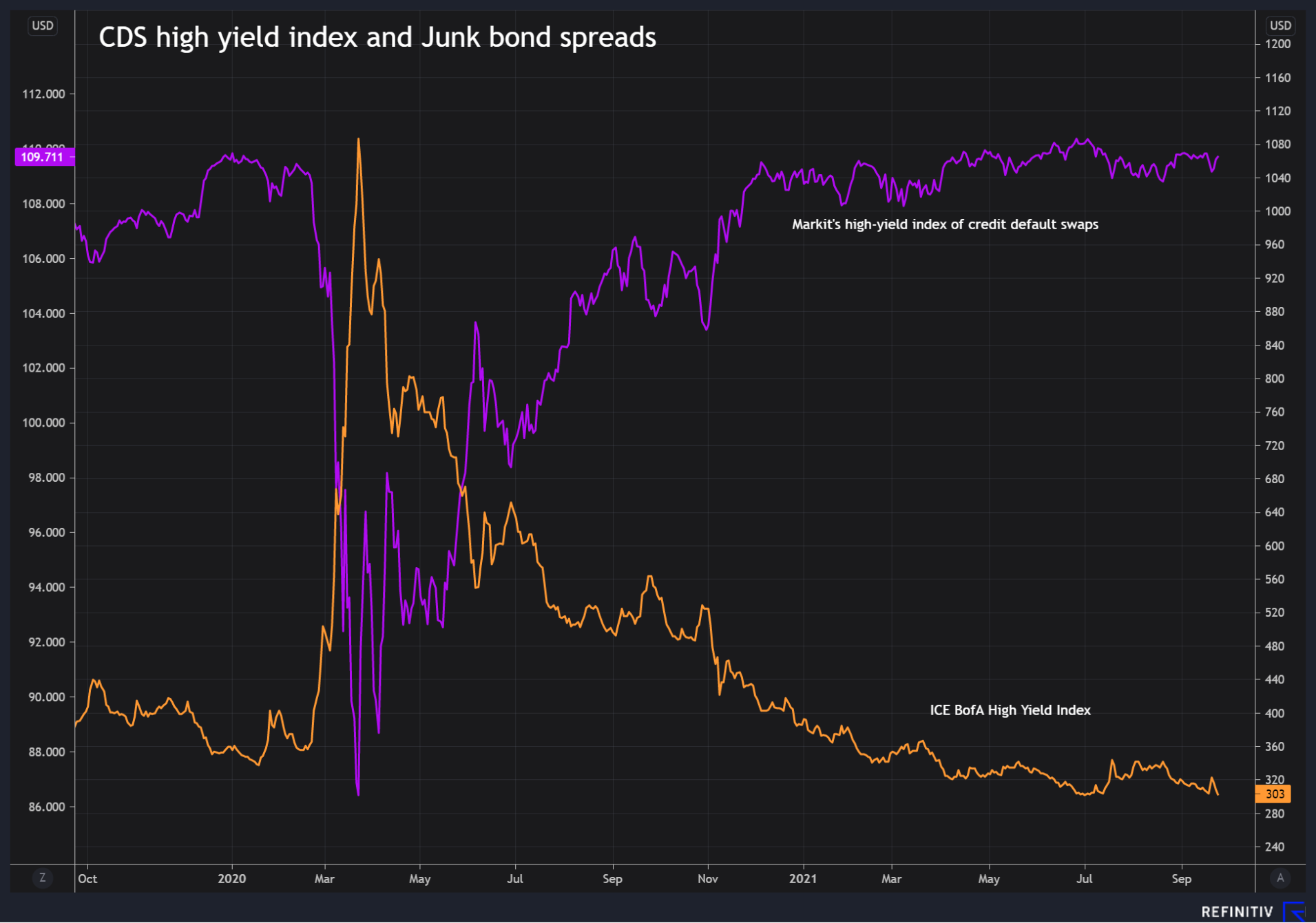

CREDIT DEFAULT SWAPS Credit default swaps provides insurance on corporate bond holdings – a way to hedge credit risk. A higher price on the CDS index, a bullish sign, indicates that investors are less concerned about potential high yield bond defaults. Markit’s high yield credit default swap index hit 109.711 on Friday and is at pre-pandemic levels.

In line with the CDS market, the spread of the ICE BofA High Yield Index (.MERH0A0) – a commonly used benchmark for the risk bond market – has narrowed, suggesting an improvement in sentiment on these assets. .

That spread stood at 303 basis points on Friday, from a pandemic peak of 1,009 basis points last year.

Reporting by Gertrude Chavez-Dreyfuss; Editing by Ira Iosebashvili and Nick Zieminski

Our Standards: Thomson Reuters Trust Principles.

Source link