[ad_1]

But these are always good times.

Do not blame the December debacle related to the partial closure of the government – it "had no significant effect on December closures," said the National Association of Realtors in its report this morning. The closure started too late in December to have a significant impact. But that could have an impact on the January closures. It will be interesting, because December was already quite painful.

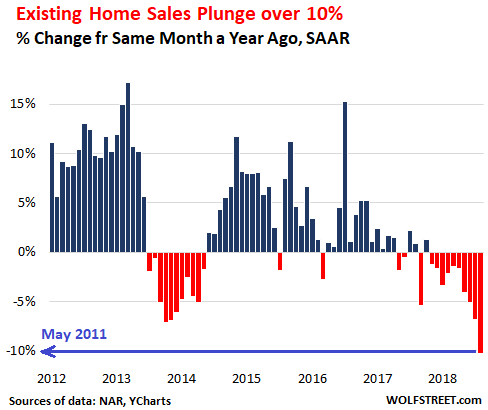

Sales of "existing dwellings" – including single-family homes, row houses, condos and co-ops – fell 10.3% in December from a year earlier to a seasonally adjusted annual rate (SAAR) of 4.99 million homes, National Association of Realtors this morning. This is the steepest decline from year to year since May 2011, during housing bust 1 (data via YCharts):

"The real estate market is obviously very sensitive to mortgage rates," says the NAR in its report. According to the Mortgage Bankers Association, mortgage rates rose 4.2% in December 2017 for a 30-year fixed-rate mortgage that averaged 5.2% at its peak in mid-November. Then, mortgage rates dropped sharply to 4.75% in mid-December.

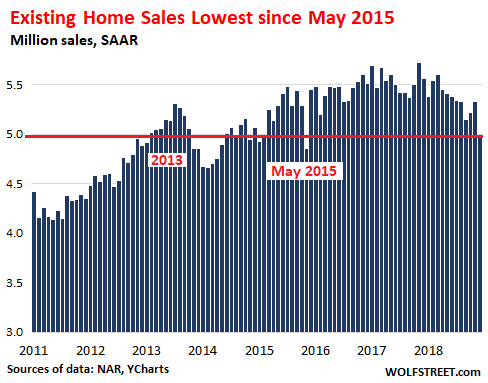

Analysts were expecting a decline in home sales, but not such a decline. The median expectation, quoted by the Wall Street Journal, was a decline in the November sales rate of 5.33 million at a rate of 5.25 million in December. The fall to 4.99 million was a kind of awakening. It was the lowest since May 2015:

By category, single-family home sales in December were down 10.1% from the previous year to a seasonally adjusted annual sales rate of $ 4.45 million. Condo sales plunged 11.5% year-over-year to 540,000 units.

Note the accelerated drop in sales of existing homes in the Midwest and the uncontrolled fall in the West:

- Northeast: -6.8%, to reach an annual rate of 690,000 inhabitants.

- Midwest: -10.5%, to reach an annual rate of 1.19 million.

- South: -5.4%, to reach an annual rate of 2.09 million euros.

- West: -15.0%, to reach an annual rate of 1.02 million.

At the end of December, the total inventory of unsold homes was 1.55 million, up 6.2% from December 2017. This is a 3.7-month supply at the rate of December sale, compared with 3.2 months a year ago. This measure of supply has been rising for seven consecutive months. And the average time spent in the real estate market has gone from 40 days in one year to 46 days.

But this growing supply is still the wrong bid – it's too expensive after years of rampant price hikes, as the NAR report said: "There is still no adequate stock for the cheapest and too many points for the most expensive points. "

The market, if it is allowed to do its job, will solve this problem by lowering prices in all areas. And very gradually, on average across the country – with prices still rising in some markets, but falling on others – this is starting to happen.

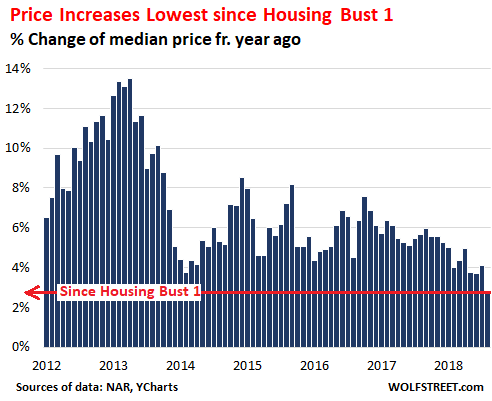

In the United States, the median selling price – meaning that half of the homes sold at more or less cheaper prices – rose 2.9% year-on-year to $ 253,600, but this was the lowest growth rate since price declines early 2012:

The median price in December was down 7.4% from June. The month of June generally corresponds to the seasonal price peak of a given year. However, the decline between June and December 2018 was the highest since 2013. In 2017, it was only 2.1%.

Median housing prices by region:

- Northeast: up 8.2% from one year to the next, to reach $ 283,400.

- Midwest: flat on $ 191,300.

- South: up 2.5% year-on-year to $ 224,300.

- West: essentially stable (+ 0.2%) from one year on the other, to $ 374,400.

Regional and national averages reflect everything that is mixed. Prices continue to rise sharply in some local housing markets. And they are declining in others. These national figures began to deteriorate as more and more local markets began to deteriorate. But this is only a slow deterioration compared to what, in many cities, was a very tight market with ridiculously inflated prices.

Housing markets are evolving slowly and are normally playing out over the years. Major sudden movements, even in local markets, are rare. At the national level, Housing Bust 1 took more than five years to come to fruition and was helped by more than 10 million job losses and a banking system on the brink of bankruptcy.

This housing slowdown came on the scene in 2018, a year in which the economy was strong and created 2.6 million jobs. This decline was triggered by dizzying prices and rising mortgage rates, not by a recession or job losses. These events – inevitable as part of the business cycle – are still waiting behind the scenes.

With the Seattle economy remaining strong, housing slowdown is not caused by layoffs or overdue mortgages. The fabulous bubble is out of breath by itself. Read … Real estate bubble problem in Seattle-Bellevue metro

Would you like to be informed by email of the publication of a new article by WOLF STREET? Register here.

Source link