[ad_1]

The decisive moment for the Bank of Japan, and the most important question for the markets boils down to this: will policymakers suggest that the side effects of monetary easing begin to worry them?

This question may reside in both geopolitics and economics.

The Bank of Japan is in a corner, especially because it may have to transfer more of its purchases of exchange-traded funds to a broader benchmark like the Topix, and far beyond the Nikkei 225, "an index of Flintsones from an abacus age," according to Nicholas Smith, analyst at CLSA

The real difficulty of the central bank lies in the bond market. Even with negative interest rates (since January 2016) and interest rate curve controls (since September 2016), the 2% inflation target for Japan remains elusive. More worryingly, the impact of these policies now threatens Prime Minister Shinzo Abe's broader gambling plan.

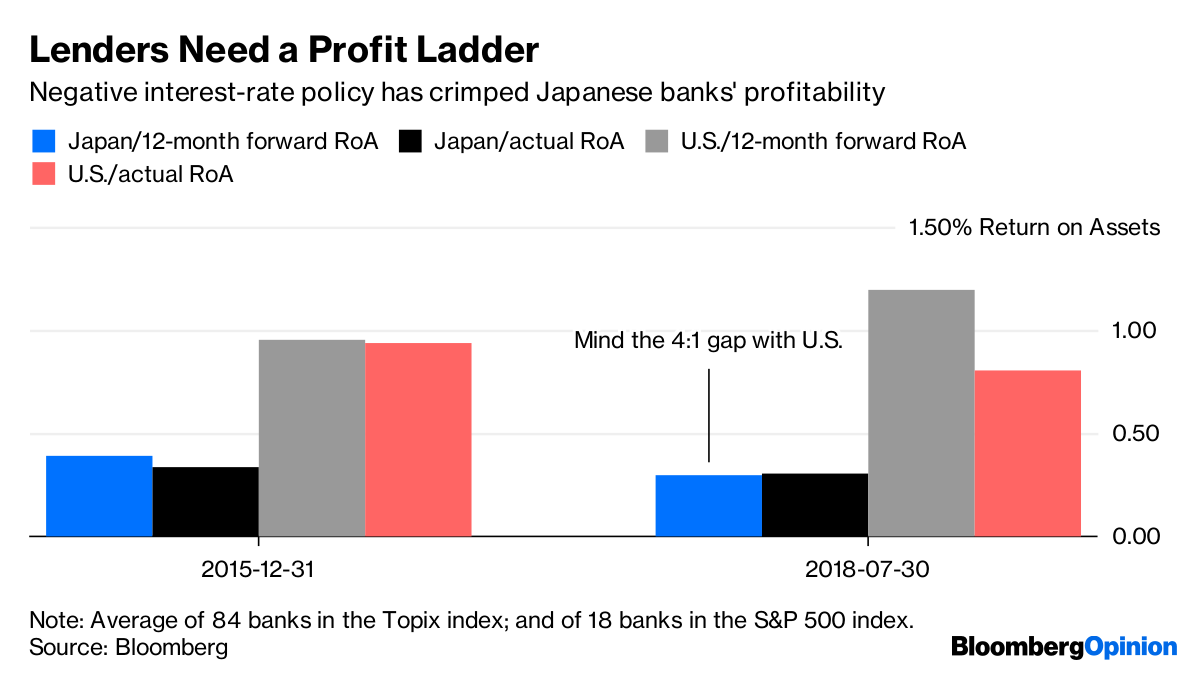

Consider the analysts 'estimate of the consensus of the one-year forward yield of the lenders' assets of the Topix Bank Index. It was 0.39% in December 2015, just before the imposition of negative interest rates. For lenders of the S & P 500 index, the expected return on investment was 0.95% in December 2015, when Donald Trump's surprise victory in the US presidential election was far from over. to be conceivable.

increase their asset yield forecasts for US lenders to 1.2%, while reducing Japanese banks' forecasts to 0.3%. What was a difference in profitability of 3: 1 is now a 4: 1 advantage in favor of Americans

Lenders need a profit scale

Interest rate policy negative has reduced profitability of Japanese banks Bloomberg

Negative interest rates have flattened the ability of Japanese banks to obtain a spread on deposits. If the Bank of Japan does not attempt to build a new profit scale, their ability to generate capital for future growth will be limited; and without this capital, they will struggle to confront Beijing's belt and road infrastructure projects in Asia and beyond.

Remember that the popular Abe appeal in the December 2012 elections was based on the promise of a big reset, which would make Japan a force in preventing its aging population from reducing the deflation and deflation. increase in the inadequacy. However, the bold monetary experience that his campaign demanded now hinders the expansion of banks, militant against the Prime Minister's goal of countering Chinese influence.

More than any threat to the stability of the Japanese financial system, this speed limit on the Abenomics is the BOJ Governor, Haruhiko Kuroda, needs surveillance

In 2017, the leading Japanese lenders – Mitsubishi UFJ Financial Group Inc., Mizuho Financial Group Inc. and Sumitomo Mitsui Financial Group Inc. – saw their plans fall by 19%. the loans for which they were the main arrangers, at $ 27 billion, even though global activity has declined by less than 3 percent, according to data compiled by Project Finance International.

The Costly Fall

The top three Japanese commercial lenders saw project loans arranged by them fell 19 percent last year; Their market share of these loans has also declined worldwide

Source: Project Finance International

One could argue that by making it difficult to make profits at home, the BOJ even pushes regional lenders like Iyo Bank Ltd. take a ride with the Bank of Japan for international cooperation supported by the state. In collaboration with the Japanese heavyweights, Iyo is also funding the construction of a hospital in Istanbul. However, a desperate search for yield in risky projects abroad may lead to credit mistakes; a boom in foreign loans backed by stable profitability at home would prove more sustainable.

What will be the exact nature of Tuesday's 'Operation Tweaks', according to analysts at Nomura Securities? Any major change in the current system of maintaining the short-term policy rate (-0.1%) and maintaining the 10-year yield of 10-year government bonds could be interpreted as the beginning of a reversal. easing, a possibility that raised his head with Kuroda's speech at the University of Zurich last November.

It may not be a bad idea, however, that the monetary authority announces greater comfort with returns at 10 years, say 0.25%, which, according to Nomura, could be a new cap. Such a change of speed could cause a temporary panic. But refusing to throw a bone to private profit banks could end up costing Abenomics more money

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners. This story:

Andy Mukherjee at [email protected]

To contact the editor responsible for this story:

Paul Sillitoe at [email protected]

[ad_2]

Source link

Tags banks BOJ bone Japan throw