[ad_1]

Three of the largest banks in the United States posted results on Friday and, for the most part, the three disappointed investors. In an article published on Wednesday of last week, I suggested that there was little to like about Citigroup, JPMorgan Chase or Wells Fargo before these reports. The fundamentals were slightly above average, the sentiment was rather bullish, and only JPMorgan Chase had a decent chart.

There is a bank reporting profits this week that I like well and that is Comerica (NYSE: CMA). The company is expected to announce its second quarter results after the closing bell on Tuesday, July 17th.

Comerica offers banking and wealth management products and services across three segments: Business Banking, Retail Banking and Wealth Management. The company operates in Texas, California, Michigan, Florida, Arizona, Canada and Mexico. Comerica is headquartered in Dallas, Texas and was founded in 1849.

Analysts expect the company to earn $ 1.64 per share for the quarter on a single figure. business of $ 833 million. The EPS estimate has not changed in the last 30 days. In the last four earnings reports, Comerica has beaten estimates of at least $ 0.05 each time.

Over the last three years, Comerica has seen its EPS increase by 21% on average per year and 51% in the last quarterly report. Sales increased by an average of 8% in the last three years and increased by 9% in the first quarter. Analysts expect the company to increase profits by 42 percent this year and 26.8 percent a year for the next five years. Comerica's profit margin is currently 39% with an operating margin of 44.9%. Both figures are well above the profit margins of Citi, JPMorgan and Wells Fargo.

Despite earnings growth, higher sales growth, higher profit margins, and higher operating margins than large banks, the sentiment towards Comerica is much less optimistic. . The current short-term interest rate is currently 2.8, which is almost twice as high as the average short-term interest of the three banks reported last week. Analysts' ratings also reflect more skepticism with only eight evaluations "bought" out of 28 evaluations. There are 18 "hold" and two "sell" ratings, which means that more than 70% of the analysts have shares listed on hold or sold. From a contrarian point of view, this leaves a lot of room for improvements.

Looking at the open option for the July options that expire on Friday, there are 8,920 open put options and 8,269 open purchase options, giving us an open month put / call report of 1.08. Looking at the August options, the ratio is approximately the same. This suggests that option traders are much more bearish towards Comerica than they were towards the big banks.

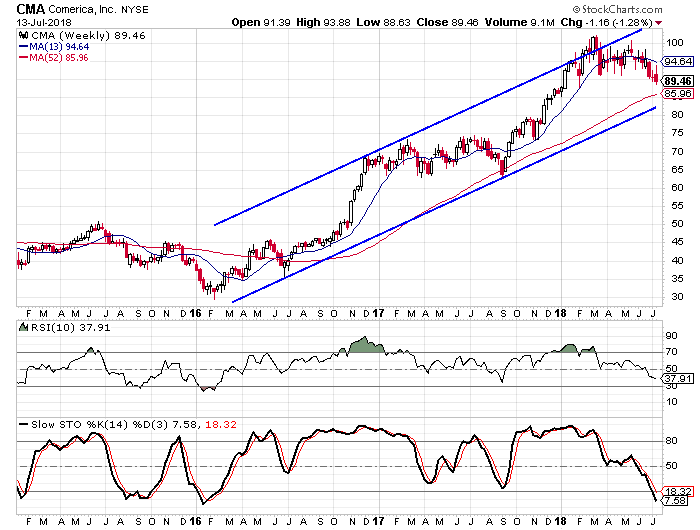

Looking at the Comerica chart, we see that the stock has been in a steady trend since early 2016. The stock has more than tripled in price over this period, but a recent lateral move has brought the oscillators down from the midpoint. For the 10-week RSI, the current reading is the lowest since last September, while weekly stochastic readings are the lowest since early 2016, just before the start of the big rally.

Another factor on the chart that I like, is that the 52-week moving average is just below the current price. The trend line provided support in withdrawals last summer and summer of '16. If the action starts to go down, I try to support it again.

Given the improved fundamentals, the more skeptical investor climate and the better chart, I wish Comerica to continue its climb after its earnings report. I do not think you need to buy it before the report, but I think there is a greater chance of a surprise up from them than about any of the banks that reported last week. I would think of longer term with this one and I would try to keep it for the next nine to twelve months and maybe longer.

Disclaimer: I have no / have no post in the stocks mentioned

I have written this article myself, and this expresses my own opinions. I do not receive compensation for this (other than Seeking Alpha). I do not have a business relationship with a company whose stock is mentioned in this article.

[ad_2]

Source link