[ad_1]

Morning news – News at 09:00 CEST

Registration link to the webinar

The dollar complied with Jerome Powell's comments deemed cautious by investors. The Fed chairman told the New York Economic Club yesterday that interest rates are now close to the "neutral" level, while he said in October that they were still far away. Powell, however, did not mention either a slowdown in the economy or the hypothesis of a pause in key rate hikes.

The pound fell against the euro yesterday, following the publication of a report by the Bank of England indicating that a UK exit without agreement and without a transition period would result in a 25% fall in the pound sterling and a GDP end 2023 more low of 7.75%10.5% compared to the projections published in May 2016.

The yen bounced this morning after the release of the excellent retail sales of October (+ 3.5% on an annual rate), suggesting an acceleration of growth in Q4.

Brent fell to a 13-month low in closing price yesterday. Oil inventories rose for the tenth consecutive week.

Today, the ECB's Financial Stability Report, Germany's Preliminary Consumer Price Index, Theresa May's Hearing, the Brexit Parliamentary Commission and the Fed Minutes will be the main ones events of the day without forgetting the G20!

NEWS THIS MORNING

Fed. Jerome Powell has been cautious in announcing that interest rates are now close to the "neutral" level while he declared in October that they were still far. Powell, however, did not mention either a slowdown in the economy or the hypothesis of a pause in key rate hikes. Jerome Powell said that rising indebtedness and declining loan quality for some US companies was one of the key weak points in the US financial system.

Brexit. According to the BOE, a Brexit without agreement and without a transition period would result in a 25% fall in the British pound, a GDP at the end of 2023 that is 7.75% lower at 10.5% than the projections published in May 2016. The report indicates that a close relationship would allow the pound to appreciate in the short term from 2% to 5%.

EU / US. Donald Trump has signaled his intention to impose customs taxes on car imports into the United States to protect the US auto industry.

Commercial War. The US administration said Wednesday that China has not made any "proposals to significantly reform" its business practices.

Japan. Retail sales growth was 3.5% in October (YoY), a record level since December 2017.

Ukraine. Two Ukrainian ports on the Sea of Azov are blocked by Russian ships, the Ukrainian Minister of Infrastructure said this morning.

APPOINTMENT OF THE DAY:

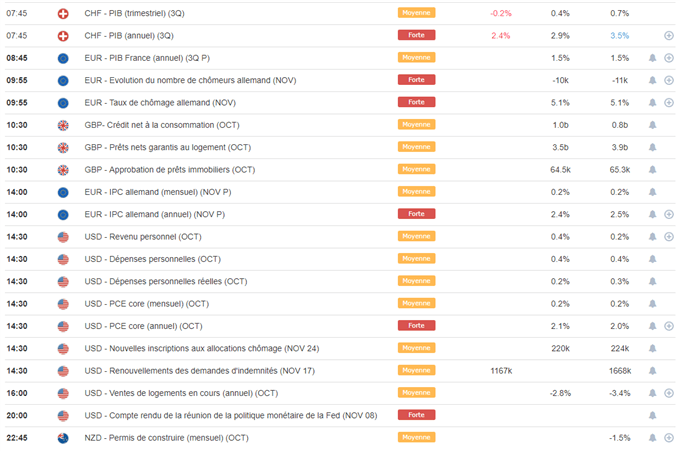

Macroeconomic calendar of 29 November 2018 from DailyFX

CONTINUE YOUR READING

The 5 dates that could calm fear on the stock markets

Since the beginning of November, major international stock market indexes such as the S & P 500, the CAC 40 and the Nikkei 225 have maintained medium-term technical support levels above which an end-of-year rally scenario can see the day.

Oil prices plummet on bottom of new restocking, the price of natural gas leaps

Oil prices resumed their decline on Wednesday afternoon as a result of the US Department of Energy's (DoE) report indicating a further restocking of crude oil last week. This is the tenth consecutive week that oil stocks have risen and this was for the fourth consecutive week higher than expected (+ 3.577Mb vs + 0.769Mb).

EUR / USD – DXY: Dollar strengthens before Jerome Powell's speech

The probability of three rate hikes of 25 bps or more by December 2019 has risen from 48% to 37% in one month. The main reason for this fall in expectations is the Fed's rate hike faster than the same economists anticipated at the beginning of the year.

Source link