[ad_1]

Background – lessons from the history of technology

I will come back to the title point in the following sections, but first, let me say a few words about my concerns about the semiconductor sector (SOX) on a time-based basis.

The Fed has been in the process of tightening for the past three and a half years, but its resolution is weakening: a dangerous pattern for cyclicals, especially with weak housing stocks and cars since more than a year.

In chips, we are witnessing major actions both technically and fundamentally deteriorating: Intel (INTC) has achieved a solid first quarter (revenue stagnant) but during the conference call, the CEO, Robert Swan, said:

The decline in memory prices has intensified. The data center inventory and capacity digestion capabilities described in January are more pronounced than expected and headwinds in China have multiplied, resulting in a more cautious IT spending environment. And yet, these same conversations with customers reinforce our confidence in improving demand in the second half of the year. So we re-evaluated our expectations for the 19's in terms of the challenges we face.

The CFO repeated:

We find that customers are becoming more and more cautious in their buying habits, the strongest deceleration occurring in China. The pressure of demand is particularly evident in our data center industry, where we are witnessing a continuous correction of inventory in business and communications, as well as a digestion of capacity in suppliers. cloud services that have significantly increased their consumption in 2018.

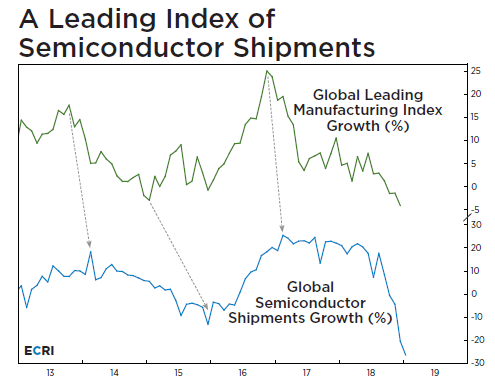

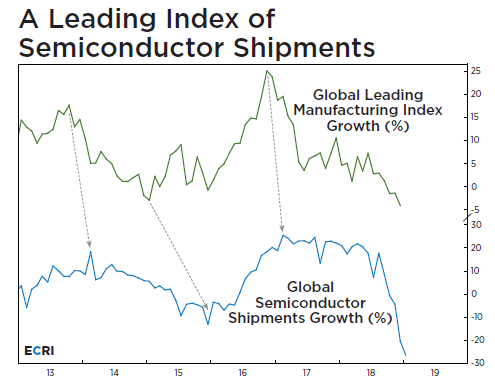

It was no surprise to ECRI, which published in March The Canary in the Semiconductor-chip Fab, in which it was found that:

The graph shows that growth in global semiconductor shipments has it's collapsedsince more than 20% since August and its growth rate has reached its lowest level in ten years.

So, my first point is that it is difficult but not impossible to synchronize technology / chip cycles, and that portfolio managers or traders with sufficiently large positions may well sell rips and falls. purchases. After buying the INTC drop last August, according to my previous INTC article, I took note, along with other data, and sold 90% of a significant INTC position in the first quarter.

Last week, I doubled that 10% position in an IRA, whether for a possible reversal or a longer-term hold. The reason for considering INTC, with its management issues and personal computer market, is that I think the Swan era at INTC might be parallel to the Satya Nadella era at Microsoft (MSFT) .

Nadella, MSFT and the return of the riders

Here, INTC seems to be about to start a race in the style of the 1980s-1990s:

INTC is not the only one to go from leader to latecomer and try to regain its former leadership status. Cisco (CSCO), led by Chuck Robbins, began a similar course at its summit, and under Mr. Nadella, MSFT is sailing in unprecedented waters. I published bullish articles on CSCO in September and February of this year, as well as on MSFT in May and again in July. I regard both actions as less cyclical than INTC and I maintain integral positions there. Each of them thrives in a new direction, and in the next section, I explore why it's a good financial bet now (the one I started to pick up) to jump into INTC or deepen it.

What Nadella did, Swan could also be doing

The Ballmer era at MSFT was not a total disaster. He was one of the first MSFT enthusiasts to establish himself in the nascent cloud and some versions of Windows were not removed.

Nadella has decided to unify the seemingly disconnected parts of MSFT into a more coherent group, focused on the Internet / network / cloud. From now on, the coherence of its sectors of activity is strengthened, the visible space allowing most segments to develop horizontally. Thus, MSFT found a premium P / E, about 25X EPS forward, much higher than that of INTC.

Nadella's MSFT is also widely touted as playing better with technology competitors / colleagues than before, and some reports suggest that MSFT's internal environment has gone from tense to pleasant.

I think these three points are where Swan wants to take INTC. To summarize:

- steer further towards software / cloud (building on hardware excellence)

- expand all parts of the sprawling INTC empire or sell them (eg, 5G modems)

- do not think like a monopoly; collaborate internally and with the rest of the technology.

The slide show of the May 8 Investor Meeting has some nuggets. For example, slide 26 of Swan's presentation explains how he wants to modify INTC:

Swan echoes Nadella as he seeks to change INTC

This slide is 4 points; my interpretations follow them, point by point:

1. INTC must listen to customers and respond to their needs instead of making products and telling them to take them.

2. Extend the playing field from about $ 50 billion to about $ 300 billion, which makes INTC a rather small (and therefore more humble) player with plenty of room to get together. develop.

3. Stop internal competition (act as a monopoly without competition) and start to behave as the challenger with a small market share. Note that this would have been a key part of the culture change at MSFT once Nadella took the reins.

4. Make sure your products are the best (for the needs of customers).

Most of them correspond to Nadella's improvements at MSFT.

To the software

Let's take a look at what Murthy Renduchintala, INTC's Director of Engineering, said in 2016 about his move from Qualcomm (QCOM) in 2015:

… With decades of experience in creating open ecosystems … integrating intelligence into unexpected peripherals, Intel is uniquely positioned to provide the full portfolio of hardware and software technologies for end-to-end intended for this purpose.[ IoT] revolution.

It may mean that he was talking about "integrating intelligence" and then mentioned software technologies on a level of linguistic equality with the material.

Now, look at the focus in his slideshow. There are 39 slides other than the 3 introductory slides and the 6 summary / closing slides. Of these, slides 18 to 33 focus on software, while slide 34 summarizes INTC's software and security capabilities. Thus, almost half concerns software.

Slide 33 says simply:

An API; to come to a developer near you in the 4th quarter of 2019.

Software, ho!

This corresponds to NVIDIA (NVDA), which revealed more than a year ago that it was using more software than hardware engineers.

MSFT remains a hardware company to a certain extent, for example. with Xbox, Surface and HoloLens, but his two major acquisitions of the Nadella era were weightless: LinkedIn and GitHub; no more Nokia phone offers (NOK) for this team. MSFT therefore remains a software / Internet / Cloud company in the first place.

I think that INTC, under the direction of Bob Swan and with the support of Dr. Renduchintala (and the board of directors), appreciates this business model and wishes to strengthen INTC's important position in the chips. (and strengthen it) by adding high value through software, including security. .

As for doing what he can with chips …

Develop the chip sector

In its communications with investors, INTC insists it is making great strides in catching TSMC (TSM) in the race for knots.

An aside: in 2014, when TSM was around $ 20 and was not much discussed on Looking for alpha, I published two bullish articles about it, Mega Cap Taiwan Semi has a quarter beat and rise; Why it is a basic technological holding company; and Taiwan Semiconductor still dominates; Purchase of the sale.

I am long TSM; However, the virtues that I have highlighted have finally been discovered. TSM, of course, has weaknesses, but thinks that the deepening process is underway.

Back to INTC and hope as part of an investment strategy.

As a small investor, I am confident that INTC can reduce operating costs and improve the performance of its chips in any way necessary. It's a big job that can have bumps even if it's successful. Customers will certainly give him time.

The remarks prepared by Swan during the teleconference left a drop of water in the wind. From the beginning, he reported that INTC considered a strong competitive response to NVDA's challenge. Praying the performance of iNTC in the first quarter, he said:

For example, the very first launch of our data-centric portfolio marked an important step in our efforts to capitalize on the opportunity of artificial intelligence and undisputed technological change. Our new second generation Scalable Xeon is the only processor in the industry to offer an integrated acceleration of artificial intelligence. Not only did we improve performance from one generation to the next, but we also showed that processor performance was better than GPU performance on major AI workloads, such as recommendation engines.

INTC claims that its processor has outperformed a GPU. Interesting! (What could Jensen Huang, CEO of NVDA?)

Whatever the case may be, INTC's broad array of chips or hardware / software solutions far exceeds the analysis capabilities of a retired cardiologist. Obviously, senior management is motivated. The question for investors is whether the street is now so skeptical and disillusioned that the chances are good for the brave investor.

I am comfortable with this bet, given the relative low value of INTC despite its many strengths in balance sheet, operations and resources.

Risks

I consider INTC, as a DJIA action (DIA), moderately risky. It is very well located in stagnating / declining industries and growing industries. But, as noted above, the flea sector is down. Any rebound in 2019 could be temporary. The opportunity of IoT things could be over-excited; Just like the TAM or the long-term competitiveness of Mobileye. And, probably at the forefront of investor concerns, INTC has simply lost his mojo, insensitive to the repair? No guarantee exists.

Conclusions – INTC, an interesting piece in the short and long term

Summing up the points above:

1. This is a difficult time for the chip companies.

2. But that means that the reduced indications of INTC can primarily reflect the dynamics of the industry, not competition.

3. In the short term, large institutional favorites, such as INTC, tend to rebound after such a sharp fall after limited negative news. INTC could therefore be a good quick exchange of long side here.

4. In the longer term, the Satya Nadella paradigm of changing MSFT's complexion for the better in many ways may be a key example that Bob Swan tries to follow at INTC. If this is correct and the execution meets Swan's expectations, points 1 and 2 above suggest that the next few months could be optimal integration periods to build, or in my case, rebuild a position in INTC.

5. Think of the triumvirate of MSFT as well as INTC and CSCO as riders of yesteryear who could all be new market stars in a new direction.

Thus, I support the proposition that INTC today could look like MSFT in 2014 with the arrival of Satya Nadella as CEO.

But as the answer has not yet been provided, the investment risk can be significant.

Thank you for reading and sharing the comments you may want to contribute.

Submitted Sunday afternoon.

Disclosure: I am / we have long been INTC, CSCO, MSFT, NVDA, TSM. I have written this article myself and it expresses my own opinions. I do not receive compensation for this (other than Seeking Alpha). I do not have any business relationship with a company whose shares are mentioned in this article.

Additional disclosure: No investment advice. I am not an investment advisor.

[ad_2]

Source link