[ad_1]

The following article is an exploration of a dataset generated from the Bloomberg terminal. He is studying Annaly Capital Management (NLY). The only reason I chose Annaly was that they went around the block several times. In other words, they have been in business since the late 90s. Most of the MREITs started after 2008. The dataset includes the following fields for the 3/29/1996 to the 26/06 / 2019.

The specific article will examine what are the main factors that affect the price. The extension whose EDF rate has an impact on the book value. I will review the modeling of the impact of Annaly's diversification efforts beginning in 2013. I will also review recent comments from management on its strategy. Originally, I had just written this article for research purposes, but I ended up adjusting my rating to buy after the recent price cut.

Description of the dataset, guide and download:

Fields directly related to Annaly: Price per share, 12-month net interest margin, dividend yield, financial leverage, quoted prices, preferred dividends, net earnings, ordinary dividends per share, outstanding shares, free cash flow , net profit applicable to ordinary shares, book value per share, EPS excluding AAP, difference in% between dividend per common share and EPS excluding AAP.

Other domains: S & P 500 ETF (SPY), FEDL01 index (tracks federal funds rates).

– preferred dividends, outstanding shares, free cash flow, net earnings and net earnings attributable to common shares are expressed in millions of dollars.

-EPS without PAA was collected by hand by consulting the press releases. These data were collected only at the beginning of 2013 because, before that, Annaly presented only GAAP.

NLY_data_set.xlsx

Attached is the dataset. If you want other fields or additional data, I will try to generate them when I find the time. I like to communicate my data to other people because you never know when you will notice a gap in knowledge. I've explored the data with the help of Tableau, JMP, R studio and Excel.

Explore the price of Annaly:

I wanted to get a first idea of the distribution of the price of Annaly on its life.

As can be seen in the histogram, there are two different frequent prices. One between $ 9-11, which we can see today, and one between $ 15-18. The average price is about 13.6 dollars, the median being slightly less than 13.14 dollars. Let's see if we can relate these prices to something, or if it's just random.

What impact on the price:

The starting point of the price is the amount of the common dividend.

The linear relationship is quite clear. The model predicts that Annaly's price will increase by approximately $ 1.2 per $ 0.1 of dividends per municipality per quarter. There is a problem with that though. Note that the long line of points is around $ 0.3 in the regression above. That's Annaly since 2013. Recently, Annaly has paid a lot of quarterly dividends around $ 0.3. Let's filter the model and see what happens.

So, if the dividend does not change, but the price always changes, what motivates the price change? Initially, I thought that dividend security would become a key factor. I've tried to model this data, but the logic does not make sense. The trend line says that the price has gone up while the dividend coverage has gone down. Why would the price increase when the dividend becomes riskier? In addition, it was not statistically significant (p-value was greater than 0.05).

I then turned my attention to the book value per share.

This seems to be the best independent variable. It's statistically significant and logic makes sense. This model is even better if you include all the dates.

This regression has a logical meaning. When the book value per share increases by 1, the price rises by about 1. Dividends are usually a determinant of price, but not as much as book value, especially in the recent future (according to the data). This does not mean that dividends are not important, but the book value per share should never be excluded, especially if price movements are taken into account.

Summary:

On the basis of this model alone, it is stated that Analy is undervalued. BV per share is about 9.6 which should be expected at a price of $ 10.5. Annaly is trading at just over $ 9.00 in action. There are many other variables that affect the price of Annaly, but the BV per share is one of the most important data I have collected.

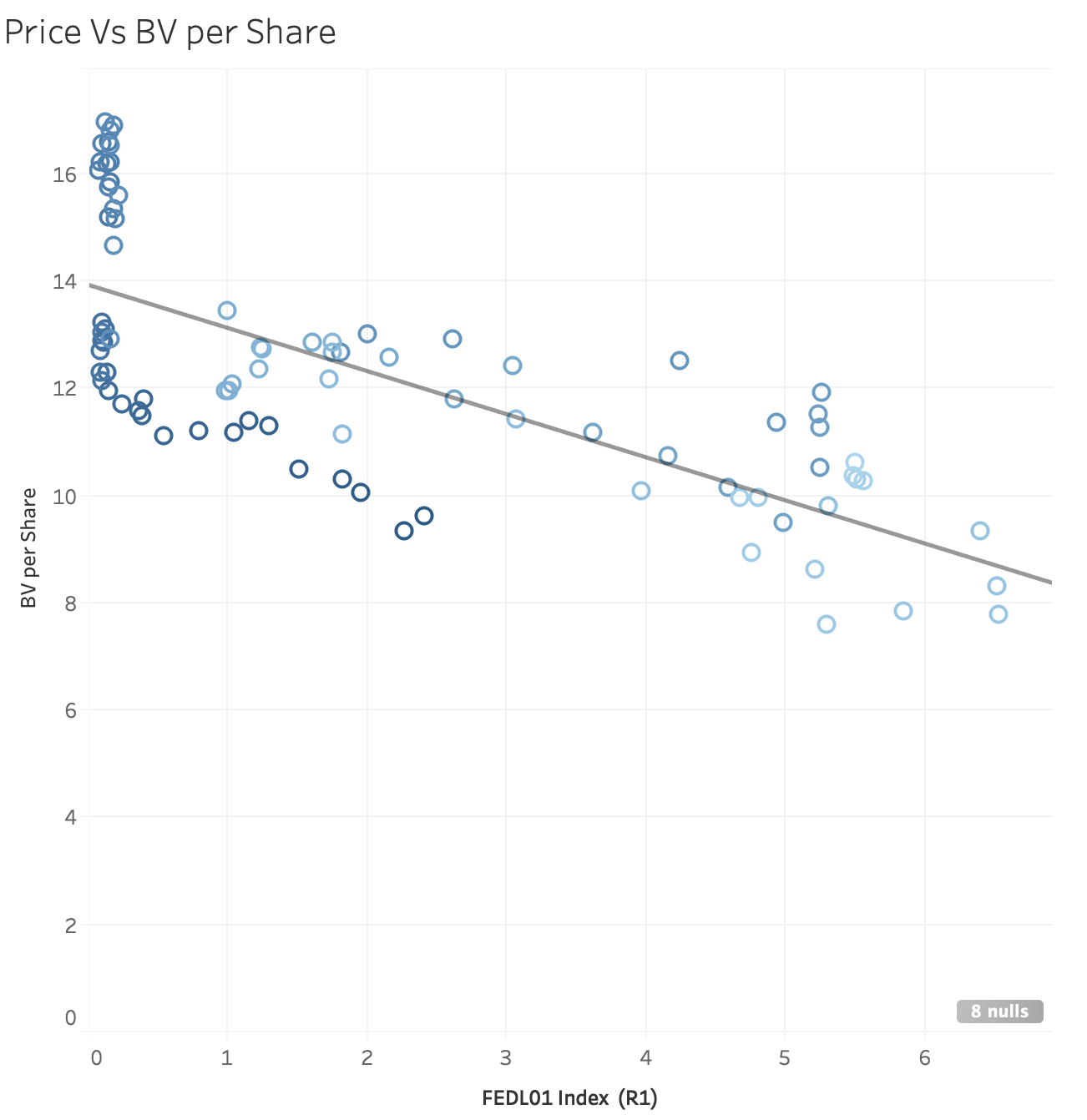

The relationship between the FED and BV:

Annaly mainly holds fixed rate mortgage-backed securities. This means that when rates rise, securities fall in book value and market value. This relationship is very strong. The correlation coefficient is about -0.75 and a value of R ^ 2 of 0.54.

This trend line indicates that when the Fed funds rate increases by 1 (100 basis points), the BV per share decreases by about 0.8. Note that the FED rate did not really have a negative impact on the risk-per-share ratio when it was close to 0. There was still movement, but it was influenced by factors that were not not present in the scatter plot.

This is not the only factor at play though. Annaly can grow BV by raising funds or enjoying the titles of his books.

Annaly & # 39; s BV increased significantly in 2011, along with the decline in Fed rates, no shares were issued. In fact, Annaly has not resumed issuing shares until the FED rate starts to increase around 2016. Emissions have now overtaken BV proportionally.

I wanted to see the relationship between the Fed's BV rate and the outstanding shares. Below you will find a multiple regression analyzing BV's change in the rate of EDF funds and shares outstanding.

Note that this multiple regression has an adj R ^ 2 of 0.94. This model also has a logical meaning. As Annaly issues more BV shares increases by about $ 11 per share. More importantly, BV drops about $ 466 million every 100 basis points, or $ 4.65 million every 1bp.

However, Annaly has changed its portfolio over time.

Source: Investor Presentation First Quarter 2019

Annaly has put more positions that have benefited from the increase in rates from 2013. Annaly has contracted variable rate loans other than agencies, MSDs, etc.. When the Fed funds rate began to rise, Annaly diversified its portfolio. I've filtered the data by date to check the effectiveness of this diversification strategy for Annaly. What I mean by that, has diversification limited the impact of the Fed funds rate on BV.

Regression Slopes: How much BV and BV per share do they change when the EDF fund rate increases by 1 (100 basis points) and the outstanding shares increase by 1.

| Book value | Shares outstanding | EDF rate (millions of dollars) |

| All data (1996 – 2019) | 10.81 | -466 |

| Before diversification (1996 – 2012) | 15.92 | insignificant |

| Only diversification (2013 – 2019) | 13.17 | -1937 |

| Recently (2015 – 2019) | 10.75 | -1236 |

| Very recently (2017 – 2019) | 12.05 | -1928 |

| BV per share | Shares outstanding | EDF rate (millions of dollars) |

| All data (1996 – 2019) | -0.001 | -0.99 |

| Before diversification (1996 – 2012) | 0.0037 | -0.68 |

| Only diversification (2013 – 2019) | insignificant | -2.15 |

| Recently (2015 – 2019) | insignificant | -1.37 |

| Very recently (2017 – 2019) | 0.0018 | -1.72 |

Regression models always have limits, but they can give us an idea of the trend.

The regression below shows a clearer picture of 2015 – 2019 and how BV per share has responded to rising rates. I've added a polynomial trend line to show the relative evolution over the years.

Annaly began to diversify in 2013, but the price / earnings per share ratio continued to decline as rates rose. It was not until 2017 that the BV per share stopped falling, even though rates were still rising. BV then continued to decline again with a recent recovery in Q1 2019.

Now that's what caused this? This is a much more difficult question to ask. I first began by isolating the short period of rate hike from 2006 to 2008. This period had only a lesser impact on the BV of only -0.49 per cent. report at -0.99 for all data and at -2.15 since the start of diversification. Prepayment may also be to blame.

Source: FHFA T4 2018 Prepayment Tracking Report

Advance payments may be partly to blame. It is true that the volatility of advance payments decreased from 2017 and remained unchanged. This could explain the first decline in BV per share, but what was the cause of the second decline and the rebound that followed? The only thing clear is that management has had mixed success.

Management Strategy:

The management of Annaly remains very positive, especially after the recent rebound of 811 million dollars of BV. This is seen in the recent call for results.

A few years ago, as rates went up and, from the outset, the federal markets took off, the market chose to choose whether you wanted to protect the book value or you wanted a return and it was difficult to provide the two. . We think that with this reset, we can – we are better placed than we are to deliver both today. Since these credit companies have evolved and we have chosen to maneuver, we can do it and move the needle quite dramatically.

Kevin Keyes, CEO of Annaly, is talking about major acquisitions here. He expects the next volatility move will put smaller companies than Annaly in trouble. Annaly will then be able to buy another company.

Conclusion:

The price of Annaly has dropped a lot recently. BV per share is below average in price and recommends a purchase. BV per share also rebounded slightly recently (around 3%). Management has had mixed success recently and Kevin Keyes seems to be moving forward with an acquisition strategy. Annaly recently announced a $ 1.5 billion stock repurchase program. This should also increase the book value per share and could even be a value for management if the price / book remains below 1 (currently 0.94).

Disclosure: I am / we are long NLY. I have written this article myself and it expresses my own opinions. I do not receive compensation for this (other than Seeking Alpha). I do not have any business relationship with a company whose shares are mentioned in this article.

[ad_2]

Source link