[ad_1]

US futures have been mixed as investors wait for the second quarter earnings season to begin this week to determine whether corporate profitability can support stock valuations. Treasury yields have fallen.

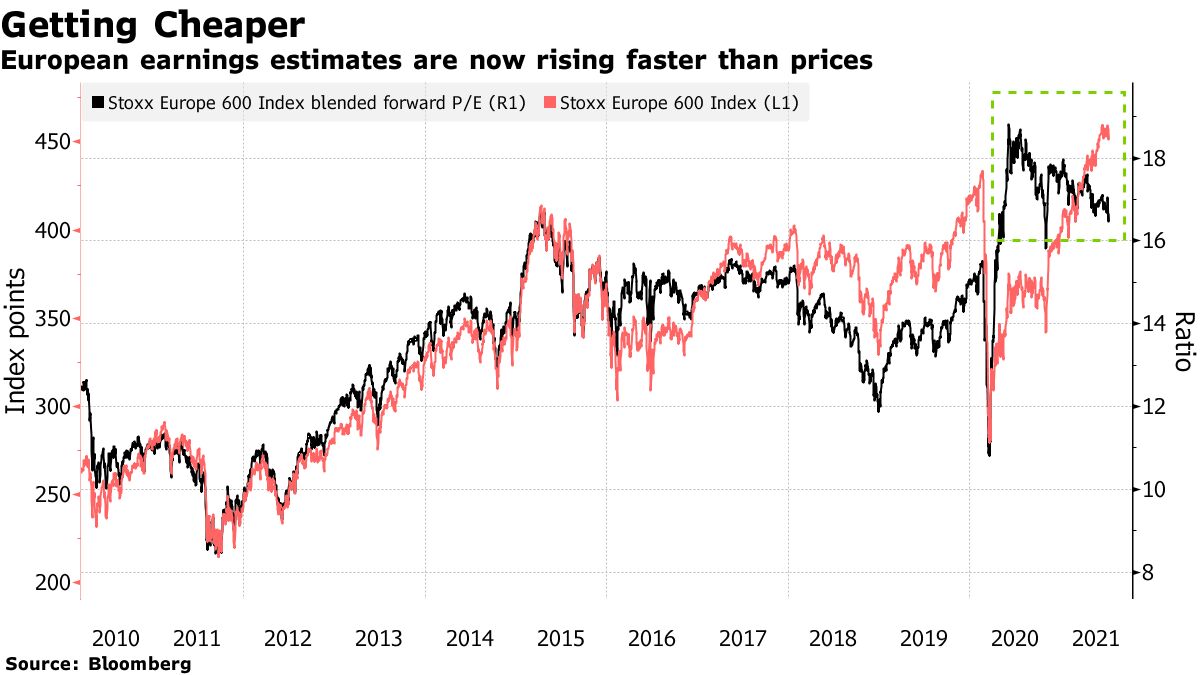

The Stoxx Europe 600 fluctuated, with declines in banks and travel agencies offsetting gains in healthcare and utilities. Atos SE plunged more than 18% after the French technology services company lowered its profit targets. S&P 500 contracts fell, while Nasdaq 100 contracts rose.

Treasuries resumed their gains after breaking an eight-session rally on Friday. They will stay focused in the middle of the news the offer hitting the market this week, along with key US inflation data and Federal Reserve Chairman Jerome Powell’s semi-annual appearance before Congress. The dollar strengthened against its major peers.

Stocks and bonds rallied amid falling long-term interest rates and inflation expectations as central banks do not rush to withdraw the support that contributed to the recovery from the pandemic . Nonetheless, investors remain concerned about the spread of the delta variant and slowing vaccination rates, while questioning when the Fed will start to gradually reduce stimulus.

“There seems to be a complacency that Goldilocks is not only alive and well, but growing stronger by the day,” Simon Ballard, chief economist of First Abu Dhabi Bank, told Bloomberg Television. “Unfortunately, we have to recognize that in the future, the longer rates stay where they are, the more we look at going down, the more severe and acute the reaction could be.”

LISTEN: Lori Calvasina, Head of U.S. Equity Strategy at RBC Capital Markets, discusses equity markets with Nathan Hager on Bloomberg Radio.

Elsewhere, Asian stocks rose earlier in the week after China’s central bank moved to increase liquidity by reducing the amount of cash that most banks need to hold in reserve to support economic growth.

The euro weakened and European core bond yields fell after European Central Bank President Christine Lagarde asked investors to prepare for new guidance on monetary stimulus in 10 days. Oil extended a decline after its first weekly loss in seven years amid an OPEC + dispute over an increase in production.

For more market commentary, follow the MLIV blog.

Here are some events to watch this week:

- Bank of America, BlackRock, Citigroup, Goldman Sachs, JPMorgan, Morgan Stanley are among the companies starting the US earnings season

- A closely watched measure of inflation – the June US consumer price index – will offer a snapshot of inflationary pressures on Tuesday

- Reserve Bank of New Zealand’s latest interest rate policy on Wednesday

- Bank of Korea monetary decision on Thursday

- China’s second-quarter GDP, main economic indicators Thursday

- Federal Reserve Chairman Jerome Powell appears before the Senate Banking Committee to deliver the semi-annual monetary policy report to Congress on Thursday

- Bank of Japan interest rate decision Friday

Here are some of the main movements in the financial markets:

Actions

- S&P 500 futures fell 0.2% at 7:14 a.m. New York time

- Futures on the Nasdaq 100 rose 0.2%

- Futures contracts on the Dow Jones Industrial Average fell 0.4%

- The Stoxx Europe 600 has changed little

- The MSCI World index rose 0.2%

Currencies

- Bloomberg Dollar Spot Index rose 0.3%

- The euro fell 0.2% to $ 1.1848

- The British pound lost 0.3% to $ 1.3856

- The Japanese yen was little changed at 110.20 per dollar

Obligations

- The yield on 10-year treasury bills fell two basis points to 1.34%

- German 10-year rate fell one basis point to -0.31%

- UK 10-year yield fell two basis points to 0.63%

Merchandise

- West Texas Intermediate crude fell 1.6% to $ 73.34 a barrel

- Gold futures fell 0.6% to $ 1,800.50 an ounce

– With the help of David Wilson, Andreea Papuc and Michael Msika

[ad_2]

Source link