[ad_1]

Fundamental Forecast US Dollar: Neutral

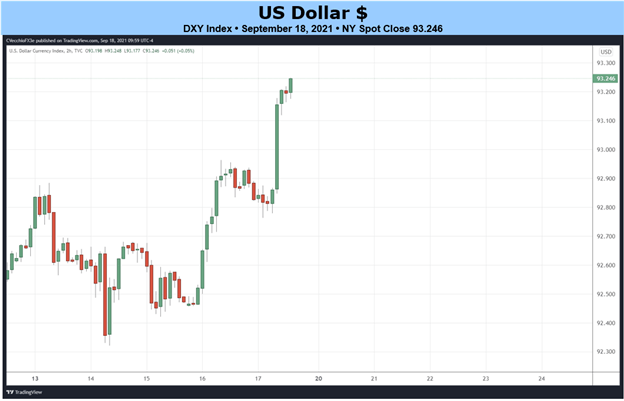

- TThe US dollar (via the DXY index) gained + 0.65% last week thanks to the Fed’s rise in ratings.

- Bond and bond markets are now the most aggressive in their hawkish expectations of the Federal Reserve all year round.

- According to the IG Customer Sentiment Index, the US dollar has a bullish bias before the September Fed meeting.

The US dollar aims higher

After a few difficult first days, tthe US dollar (via the DXY index) gained + 0.65% last week thanks to the Fed’s rating hike. Bond and bond markets are now the most aggressive in their hawkish expectations of the Federal Reserve all year round. The largest component of the DXY index, EUR / USD rates, fell -0.71%, while USD / JPY rates gained + 0.09%, hampered by weak equity markets .

Elsewhere, the greenback’s gains were equally if not more pronounced: GBP / USD fell -0.69%; AUD / USD fell -1.18%; NZD / USD fell -1.06%; and USD / CAD added + 0.65%.

Busy US economic calendar, eyes on Fed meeting

Mid-September will produce another loaded US-based event risk case. Of course, many data releases could be reduced in importance, as the September Fed meeting overshadows everything else.

- At On Monday, September 20, the The September NAHB US Housing Market Index will be released.

- On Tuesday, September 21, August data on US building permits and US housing starts are expected.

- On Wednesday, September 22, weekly US MBA mortgage applications and US existing home sales in August will be released in the morning, while the September Fed meeting and President’s press conference of the Fed, Jerome Powell, will take place in the afternoon.

- Thursday, September 23, the August national activity index of the Chicago Fed in the United States, the weekly jobless claims figures, the September American Markit manufacturing PMI (flash) and the American CB leading index d August are all expected.

- On Friday, September 24, the August US New Home Sales Report will be released and Fed Chairman Powell will deliver a speech.

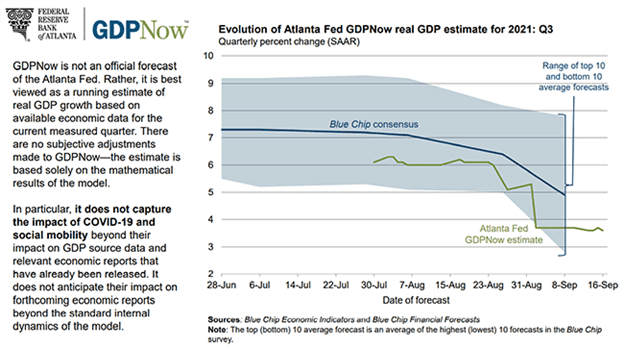

Atlanta Fed GDP growth estimate for Q3’21 (September 17, 2021) (graph 1)

Based on the data received so far on 3Q’21, Atlanta Fed GDPNow the growth forecast has been revised downwards from + 3.7% to + 3.6% on an annualized basis. It was because “a decrease in the immediate forecast for growth in real gross private domestic investment in the third quarter compared to +19.2% to +18.9% was partially offset by an increase in the nowcast for real personal consumption expenditure growth in the third quarter compared to +2.1% to +2.2%, while the immediate estimate of the contribution of the change in real net exports to real GDP growth in the third quarter fell from -1.41% to -1.37%.“

The next update to the Atlanta Fed’s GDPNow growth forecast for 3Q21 is expected on Tuesday, September 21.

For full American economy forecast data, display DailyFX Economic Calendar.

The bond market expects a hawkish Fed

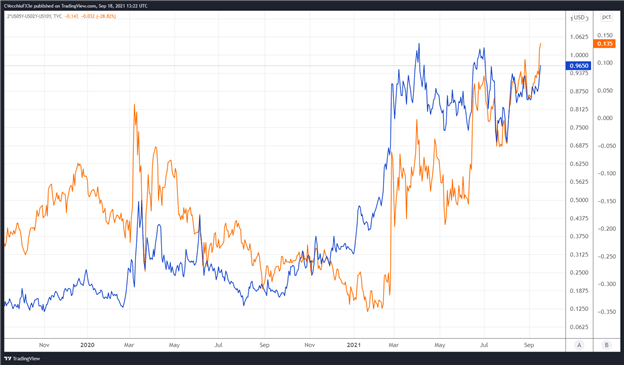

We can measure whether a fed The rate hike is integrated into the price using Eurodollar contracts by examining the difference in borrowing costs for commercial banks over a specific time horizon in the future. Chart 1 below shows the difference in borrowing costs – the spread – for the September contracts of 2021 and December 2023, in order to assess the evolution of interest rates in the interim period between September 2021 and December 2023.

Spread of Eurodollar futures (September 2021-DECEMBER 2023) versus the American butterfly 2s5s10s: daily rates graph (September 2019 to September 2021) (graph 2)

We can overlay the Fed rate hike ratings with the US Treasury’s 2s5s10s butterfly to determine whether or not the bond market is acting in a manner similar to what happened in 2013/2014 when the Fed started. to move forward with its reduction plans. The butterfly 2s5s10s measures non-parallel changes in the US yield curve, and if the story is correct, that means intermediate rates are expected to rise faster than short or long rates.

Indeed, while the Fed’s rate hike ratings were largely unchanged after the July FOMC minutes – which clearly indicated the line between the rate cut and rate hikes – we can see that the U.S. yield curve is moving in a way that suggests a more hawkish Fed is here. While there are 97 basis points of discounted rate hikes through the end of 2023, the 2s5s10s butterfly hit its highest rate since the Fed’s tapering talks began in June 2021, and its highest overall level since June 2018.

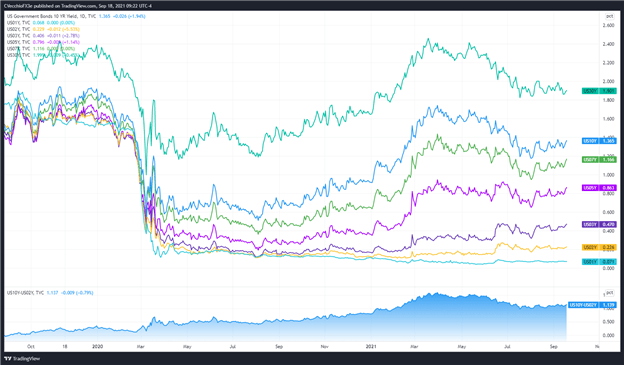

US Treasury yield curve (1 to 30 years) (September 2019 to September 2021) (Chart 3)

Historically speaking, the combined impact of rising US Treasury yields – particularly as middle rates outperform short and long rates – along with the Fed’s high rate hike ratings created a more favorable business environment for the US dollar .

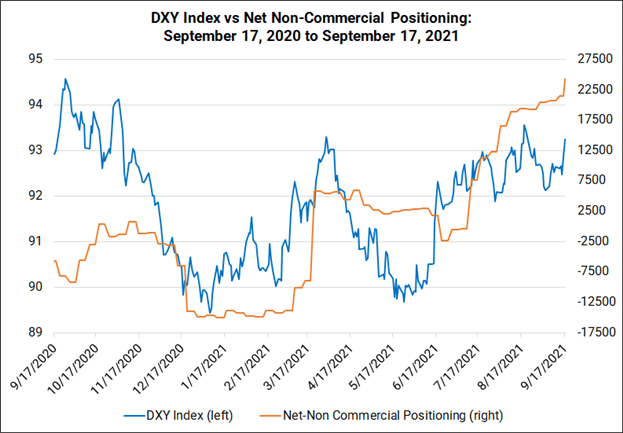

CFTC COT positioning on US dollar futures contracts (September 2020 to September 2021) (Chart 4)

Finally, in terms of positioning, according to the CFTC’s TOC for the week ended September 14 speculators increased their net long positions in the US dollar to 24,244 ccontracts out of 21,458 contracts. The net long positioning of the US dollar remains near its highest level since the last week of November 2019.

— Written by Christopher Vecchio, CFA, Senior Currency Strategist

[ad_2]

Source link