[ad_1]

Wall Street hype artists and various QE dealers would be deeply disappointed.

Lael Brainard, Governor of the Federal Reserve, spoke at the heart of his presentation on "How is monetary policy affecting your community?". It was under the subtitle "Some questions to explore". the next crisis will be treated.

In the next crisis, when short-term interest rates will already be zero – for the Fed, this remains the lower limit – the Fed might not apply the kind of quantitative easing that it had done during and after the financial crisis when she had set a goal of buying a fixed amount of securities each month.

During the next crisis, when short-term interest rates (0%) will no longer be enough to stimulate the economy, the Fed could announce a goal of slightly longer rates, such as interest rates. a year, said Brainard. And she would buy just enough securities with these deadlines to bring the one-year return back to the target range. And if more stimulus is needed, this could target two-year rates, she said:

Under this policy, the Federal Reserve would be willing to use its balance sheet to reach the target interest rate, but unlike the asset purchases undertaken during the recent recession, there would be no specific commitment with respect to purchases of Treasury securities.

"Such an approach could help publicize how long the Federal Reserve plans to keep rates low," she added.

It's an "interest rate pegging": been there, done that.

For example, the Fed would like the return of one year to be 1%. If the Fed is credible in its announcement, it may not need to buy a lot of securities to get the return of a year.

Brainard said, "This is just one of the 'ideas', and there may be other good ideas. Part of the process we are engaged in is looking for other ideas. "Nevertheless, the test ball floats.

The Fed had already set up an anchor rate previously to help provide inexpensive funding to the US war effort during the Second World War. The Fed tells this episode:

The interest rate setting came into effect in July 1942 and lasted until June 1947. Reserve banks reduced their discount rate to 1% and created a preferential rate of 0.5% for loans. guaranteed by short-term government bonds, well below the 3 to 7% that was common in the 1920s.

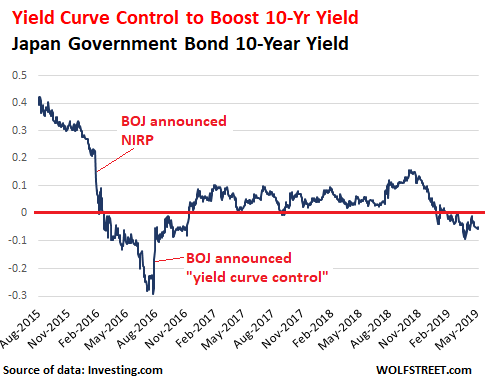

The Bank of Japan has a rate anchor.

In many of the central bank's strategies to control or manipulate markets directly or indirectly, the Bank of Japan has been at the forefront. The BOJ was conducting a quantitative easing program – even though it did not call it that – long before the Fed launched its quantitative easing program in late 2008. Then, in 2016, the BOJ launched its rate curve targeting program, which it dubbed "controlling the yield curve," program by which it attempts to control the entire yield curve , including 10-year returns.

The Japanese yield curve became a problem at the end of December 2015, when the 10-year yield began to plummet following rumors that the BOJ would apply a negative interest rate policy. In February 2016, when the BOJ confirmed the rumors and announced its NIRP policy, the 10-year yield plunged further, crossing the zero line and becoming negative. And the already languishing Japanese banks were crying.

At the end of July 2016, when the 10-year yield fell to -0.29%, the BOJ announced its "yield curve control" program: it wanted the 10-year yield to be close to 0% but above. The 10-year yield climbed from -0.29% to -0.08% and continued to increase until it was above 0%. The BOJ fulfilled this task in jawboning but also in do not-buy or perhaps even sell long-term securities. It was the opposite of the Fed's Twist operation.

It worked uneventfully until the end of 2018, when the BOJ – motivated by trade tensions, the global slowdown in the manufacturing industry, and the Fed's "patience" – allowed the 10-year yield to drift slightly in the disturbing (data via Investing.com):

A tariff clamp has an "automatic exit": Bernanke

There have been voices that have discussed a rate setting option, including Ben Bernanke in March 2016, after he was no longer chairman of the Fed:

To illustrate the operation of an anchor, assume that the overnight rate is at zero and the two-year Treasury rate at 2%. The Fed could announce its intention to keep the two-year rate at one per cent or less and enforce that ceiling by preparing to buy any Treasury stock with maturities of up to two years at a price equal to one per cent. yield of one percent.

The price of a bond being inversely proportional to its yield, the Fed would indeed propose to pay more than the initial market value. Think of it as price support for a two-year public debt.

Timing details are important. Suppose the Fed announces on May 1, 2020 that it is ready to buy any Treasury securities maturing May 1, 2022 or earlier at fixed prices corresponding to a 1% return. Note that, with time, May 1, 2022, the deadline will not change (unless explicit extension); thus, the maturities of securities that the Fed is committed to buying would decline over time and the program would automatically end at the specified end date.

And here, Bernanke explains how this form of quantitative easing would unfold automatically:

In addition, all securities purchased by the Fed under this program would mature on the deadline, which will have no lasting impact on the Fed's balance sheet. This "automatic exit" is an attractive aspect of the approach.

This approach of QE by anchoring rates do not be designed to inflate asset prices, in contrast to the conventional QE that has been specifically designed to inflate all asset prices to create a "wealth effect".

A rate setting of this type is aimed at making the loan cheaper along certain parts of the yield curve, while minimizing the number of securities the Fed should buy to do so. In addition, with the "auto-exit" feature, persistent problems caused by traditional EQ would no longer occur. Wall Street threshing artists and various QE resellers who have been demanding QE for months would be deeply disappointed by this rate-pricing approach rather than a proven true QE.

The Fed withdrew $ 46 billion from its balance sheet in April, while total QE Unwind reached $ 580 billion and its assets dropped to their lowest level since November 2013. Read... The Fed's QE continues at full speed in April

Do you like to read WOLF STREET and want to support it? Using ad blockers – I fully understand why – but you want to support the site? You can give "beer money". I like it a lot. Click on the beer mug to find out how:

Would you like to be informed by email of the publication of a new article by WOLF STREET? Register here.

[ad_2]

Source link