[ad_1]

The rate cuts for 2019 are just a dream: Goldman Sachs and Deutsche Bank.

That's now two: Chief economists at investment banks Goldman Sachs and Deutsche Bank have warned their clients that the rate hikes already built into this year's price and that spark so much excitement over markets may not materialize.

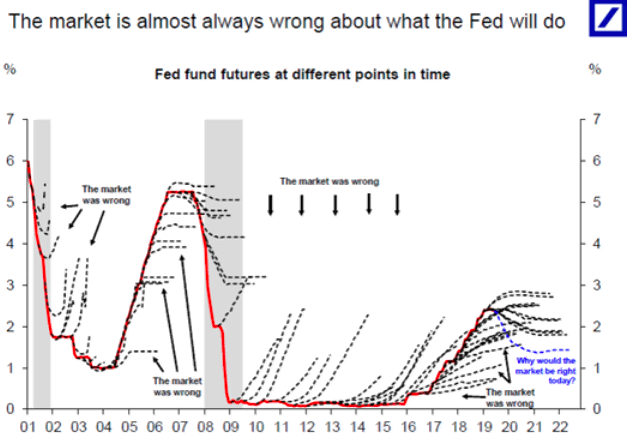

To prove their point, Deutsche Bank's chief economist, Torsten Slok, and his team analyzed the data back to 2001 by comparing the evolution of the federal funds rate – which reflects increases and decreases rate hike – to the federal funds rate futures markets. . They concluded: "The market is almost always wrong to know what the Fed will do."

And they asked, "Why would the market be right today?" It was a rhetorical question.

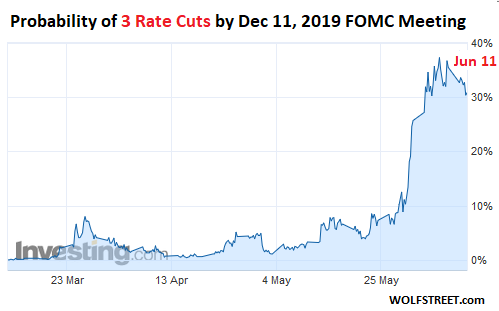

Yet these bets – which are "almost always wrong" on the Fed's rate decisions – are now being quoted all the time to show that the Fed will reduce its target range for federal funds rates. For now, these traders see an 80% probability that the Fed will reduce its target range at least twice at the December 11 meeting, with a 31% probability three cuts from here, and a probability of 10% four cutsas implied by the negotiation of 30-day federal futures contracts.

This graph shows how three rate cuts have suddenly increased in Fed Funds futures traders on the CEM, although they have declined slightly over the past two days (graph via Investing.com). :

Whenever traders in Wall Street rate cuts can turn something that a governor says the Fed into a rate cut forecast, they will do it. For example, Fed Chairman Jerome Powell delivered a speech on June 4 on long-term issues the Fed is thinking about. The speech was not related to what the Fed will do in future meetings. Outside of his context, he launched this line – "we will act appropriately to support the expansion" – at the beginning.

The low-rate walkers took this line to affirm the reduction expectations of the three rates. Yet no talk of imminent rate cuts was spoken in this speech. That the Fed "behaves appropriately" is the standard jargon of the Fed to describe the fact that the Fed is awake. It can go both ways, hiking or cutting.

This is how the Deutsche Bank team published this chart (via Bloomberg) entitled "The market is almost always wrong about what the Fed will do", where they compare what the rate of federal funds (red line) actually did. what the futures trading on Fed funds said it would do (dashed black lines):

From 2001 to 2004, Federal Funds Futures provided that the Fed would raise rates. But the Fed has continued to lower rates. Then, when the Fed finally began raising rates, federal funds futures had planned to stop raising rates at any time. False, false, false. Etc.

Over the years of ZIRP, federal funds projected future rate hikes, and they were deceived there until 2016, when the Fed finally began raising rates. has started.

The blur of the dotted blue line from 2019 in the future shows the Fed's market orientation. And the Deutsche Bank team observes (in blue): "Why would the market be right today?"

In other words, the market has no idea of the Fed's future rate decisions. He has his own reasons to bet as he does, but not to make an accurate projection of where the Fed is heading with its interest rate target.

And yesterday, it was Jan Hatzius, chief economist of Goldman Sachs, quoted in a note cited by CNBC. He clearly understood the market interpretation of the line of act as Powell.

Without this line, the discourse "exclusively focused on long-term issues, while trade policy was raising growing concern, might otherwise have seemed" disconnected "from some market players," he writes.

"In our opinion, this was not a significant indication of a future reduction, but was simply to reassure the FOMC about the risks of the trade war."

Goldman Sachs expected the Fed's governors "to be very careful not to deliver an unconditional hawkish message, but to continue to stress that they will respond to the shocks needed to carry out their mandate."

Given that the FOMC meeting in June will be held just before the G-20 summit, where Trump hopes to meet Chinese President Xi Jinping on the sidelines and the uncertainties surrounding it, "the right solution is to retain the character optional "Hatzius writes.

He expects the FOMC to slightly degrade the economic outlook at the June meeting, with some participants indicating that they may be in favor of rate cuts, but that the median forecast of the dot chart for the target range for the federal funds rate will remain unchanged. there will be "no signal from Powell that a break is imminent".

Hatzius wrote the following for the remainder of the year 2019: "While this is a close decision, we still expect the FOMC to keep the fund rate unchanged for the rest of the year.

But if there is no rate cut, even though the stock market and the Treasury securities market have jumped in the face of expectations of two or three rate cuts, somehow will have to progressively denigrate the markets – if not. And maybe Goldman Sachs is trying to lay the groundwork.

At present, the stock market and the corporate bond market are at home, experiencing only economic growth. They are calling for rate cuts. But they do not see a low-rate economy. So, why the Fed? Read … Here's my prediction: if the Fed does not cut rates 3 or 4 times by December 11, markets will get lost

Do you like to read WOLF STREET and want to support it? Using ad blockers – I fully understand why – but you want to support the site? You can give "beer money". I like it a lot. Click on the beer mug to find out how:

Would you like to be informed by email of the publication of a new article by WOLF STREET? Register here.

[ad_2]

Source link