[ad_1]

Growth in the services sector slowed last year but remains strong.

Based on the 30-day federal funds futures prices for the moment, the market sees a 57% probability that the Fed will reduce rates one notch or so up to its December 11th meeting. The market sees no measurable chance of rate hikes. The Fed would generally cut rates because the economy is in trouble. So, let's see.

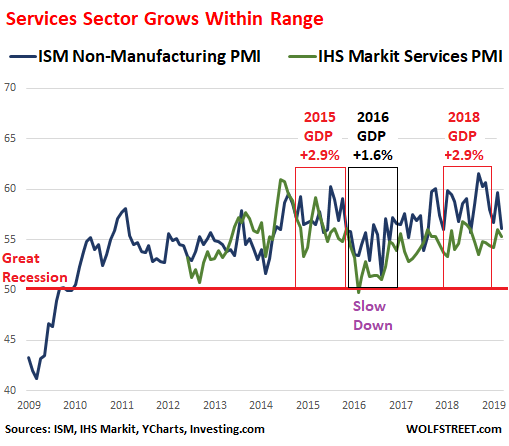

The services sector, which accounts for about 70% of the US economy, lost ground to hot flashes that occurred for short periods in 2018 and were similar to those of accelerated growth in 2015. In 2015 and 2018, "Real" GDP (adjusted for inflation) rose 2.9%, the fastest growth since the Great Recession. And the latest data show that the economy is coming back from the top of the range in the middle of the range.

This was confirmed this morning by two reports on the services sector in March, the non-manufacturing ISM report and the IHS Markit US Services PMI. Both are indices where a value greater than 50 indicates growth and a value less than 50 indicates a contraction in the service sector. The higher the value, the faster the growth.

ISM non-manufacturing index, at 56.1, records solid growth but has already given way to the strong growth spurts of September, October and November 2018, when the index levels had exceeded 60. The index also exceeded 60 in October 2017 and July 2015. These 60 readings are therefore not very common. The ISM non-manufacturing index is now back in its normal post-financial crisis range.

The IHS Markit US Services PMI, at 55.3, "Reported a new strong growth in business activity in the US service sector," says the report. "The increase was slightly lower than in February, but it was nevertheless supported by a sharp increase in new orders and a new recovery of new business from abroad."

The chart below shows the two indices: the non-manufacturing ISM index (blue line, via Investing.com, up to 2009) and the IMS Markit Services PMI (green line, via YCharts, up to 39). ;in 2012). I have marked the two strongest years of growth in red, 2015 and 2018, when GDP grew by 2.9%; and the year of the slowest growth in black in 2016, when GDP recorded a gain of only 1.6%, while the property-oriented sectors have entered a decline accentuated by the effects of the economy. 39, collapse of oil. In March 2016, the IHS PMI index fell below 50, and consequently in contraction mode. But that did not last and the service sectors took off again:

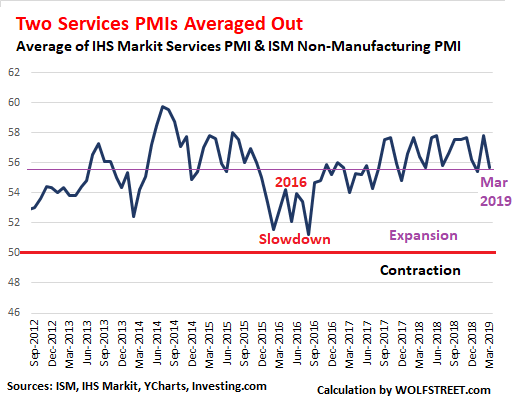

The non-manufacturing ISM PMI and the IHS Market Services PMI follow the broad economy of services in different ways and do not include all the same sectors.

The IHS Markit PMI is narrowerIt includes consumer services (except retail), transport, information, communication, finance, insurance, real estate and business services.

The ISM PMI is larger: This includes retailing; construction; professional, scientific and technical services; Health care; educational services; accommodation and catering services; public administration; mining; business services; agriculture, forestry, fishing and hunting; transportation and storage; real estate, rental and leasing; information; arts, entertainment and recreation; public services; finance and insurance; and wholesale.

So I did something that I would have done better not to know how to do, but I was at home alone, so to speak: I averaged both indices ( adding the data points of the two indices for each month since 2012 and dividing the results by two). This eliminates some of the noise and shows more clearly the trend, including slower growth in the service sectors in 2016 and the return to the middle of the growth range set after the 2016 downturn:

Beyond the global ISM non-manufacturing PMI, are the sub-indices. Of the three main sub-indices, two showed slower growth:

- Business activity index of non-manufacturing companies (57.4% in March vs. 64.7% in February)

- New orders index (59% in March, versus 65.2% in February).

And one of them showed a growth in acceleration.

- Index of employment (55.9% in March, after 55.2% in February).

Of the 18 individual sectors covered by the ISM index, 16 posted growth in March and two outsourced (education and retail services).

The IHS Markit report notes that companies have linked the recovery of activity "to strong customer demand":

The increase in new orders was attributed to increased demand from new and existing customers. Although the pace of growth was slightly below the trend of the series, it is one of the strongest in the last five months. At the same time, new export activity increased for the second month in a row, often due to the acquisition of new customers.

The backlog increased for the third month in a row and "the backlog accumulation rate was the fastest since November 2014 and solid overall".

But the prospects for production for the next 12 months have been overshadowed by "concerns over uncertainty over global trade tensions, concerns about economic growth and more intense competition. The level of optimism has fallen to the lowest since December 2017 and has been reduced overall. "

And job creation "has slowed to the lows since May 2017, partly because of declining business confidence."

So that's the kind of scenario where everything is not crazy, but overall, business is on track for solid growth, with real strengths in some areas and weaknesses in others.

If service activities falter, as was the case in 2016, the Fed will become nervous about the economy. But if service activities remain in the current range, the Fed may feel emboldened. Even the FOMC doves have expressed their belief that with the current economic context, the moment is not conducive to a reduction in rates. And others, given the current economic situation, have proposed a rate hike. And the service sector will be the key to the development of the plot.

In the manufacturing sector, the weakness is global, but the United States, the cleanest dirty shirt among the giants, hold on, thinking that their shirt becomes dirtier. Lily... US shirts still the cleanest among the giants of the manufacturing sector, Germany falling to the levels of the debt crisis, contracts with Japan, China relies on the government's private sector rescue

Do you like to read WOLF STREET and want to support it? Using ad blockers – I fully understand why – but you want to support the site? You can give "beer money". I like it a lot. Click on the beer mug to find out how:

Would you like to be informed by email of the publication of a new article by WOLF STREET? Register here.

[ad_2]

Source link