[ad_1]

Exports at cost price for economic growth are coming home.

The manufacturing industries of the major manufacturing countries, especially those focused on exports, have reached varying levels of discomfort, ranging from slowing growth to panic-triggering declines, according to manufacturers 'purchasing managers' indices published in May. , published Monday. PMI data show that manufacturing in the United States is growing more slowly, but continues to grow. The United States continues to be the cleanest dirty shirt in this group.

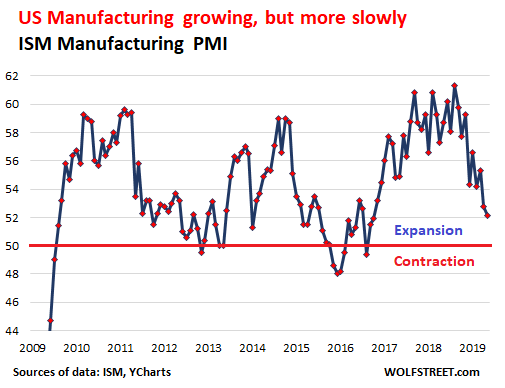

The US Manufacturing PMI released by the Institute of Supply Management for May, released this morning, showed that economic activity in the US manufacturing sector had increased in May but at a slower pace. As for all these PMIs, a value greater than 50 indicates an expansion, and the higher the value is greater than 50, the faster the rate of expansion. A value less than 50 indicates a contraction. The ISM manufacturing PMI for May was reduced to 52.1 (data via YCharts):

"The panel's comments reflect the growing strength of the company, but at low levels," the report says. "Respondents expressed concern over the escalating trade stalemate between the US and China, but the overall sentiment remained broadly positive."

Here are some key points:

- "The expansion of demand continued with the strengthening of the new orders index" at 52.7, but it remained in a slow growth mode, namely "the weakest of the 50s".

- The unfilled orders index was contracted for the first time since January 2017 and grew quite sharply, falling from 47.9 to 47.2.

- The index of production rose but at a slower pace, to 51.3 (vs. 52.3 in April).

- The employment index rose faster, reaching 53.7 (vs. 52.4 in April).

Of the 18 manufacturing industries covered by the ISM PMI, 11 recorded growth in May:

- Printing and related support activities;

- Furniture and related products;

- Plastic and rubber products;

- Textile factories;

- Miscellaneous manufacturing;

- Electrical equipment, apparatus and components;

- Computer and electronic products;

- Chemical products;

- Food products, beverages and tobacco;

- Non-metallic mineral products;

- Machinery.

And six of the 18 industries reported a contraction in May:

- Clothing, leather and related products;

- Primary metals;

- Petroleum and coal products;

- Wood products;

- Paper products;

- Manufactured metal products.

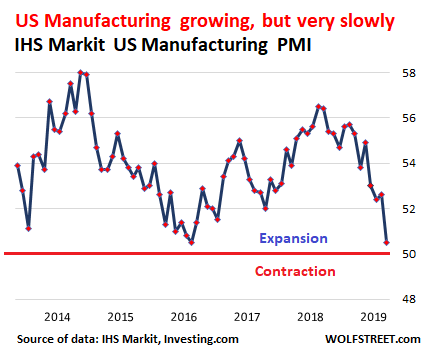

The US manufacturing sector is also covered by the IMI Markit US Manufacturing PMI, released this morning, for a slightly different point of view. It still posted growth (50.5%), but the lowest growth since the Great Recession, "as production growth slowed and new orders fell for the first time since August 2009".

Employment has increased, but at the lowest rate since March 2017, "in a tense job market context".

Production increased only marginally, "often related to the absorption of orders waiting for past orders".

New orders fell for the first time since August 2009. "Although only a very small amount, survey respondents said that weak customer demand led to the fall. Some companies also noted that customers were deferring their orders due to growing uncertainty about the outlook. New orders from abroad contracted, "at a marginal pace," for the first time since July 2018.

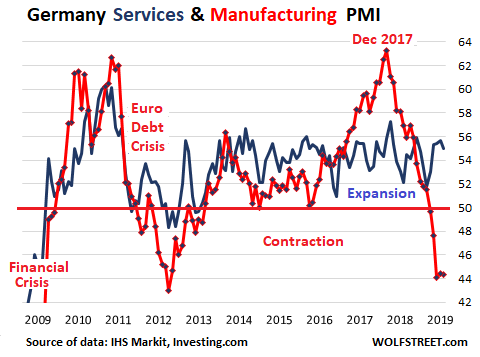

German manufacturers, the saddest and most sinister.

The legendary dependence of the German economy on the manufacturing sector for exports, and in particular its automotive sector, has certain drawbacks when the automotive sector generally decreases, as is currently the case, and exports deteriorate in general.

The IHS Markit / BME Germany manufacturing PMI continued to contract, at 44.3%, the strongest contraction for all manufacturers.

However, the German PMI of services has been high and the gap between services and the manufacturing sector is striking. The graph below shows the deplorable situation of the manufacturing sector (red line) and the strength of the service sector (blue line, IHS Markit Services PMI). Even in Germany, services (including healthcare, finance and insurance, information services such as data processing and telecommunications, and professional services such as lawyers and architects) by far the largest part of the economy.

"Stronger Growth in the Consumer Goods Sector" Helped to Mitigate the Decline in Manufacturing Output for the Second Consecutive Month, Also Assisted by "Slower Decline in Equipment Goods" . The contraction in the strongest output has occurred among manufacturers of intermediate goods.

Despite easing, the latest declines were broadly marked, anecdotal evidence highlighting the effects of the slowdown in the auto industry, the US-Chinese trade conflict and customer destocking on sales.

And the manufacturing job takes a hit. Manufacturers fired workers for the third month in a row: "After accelerating the slow rates of decline observed in March and April, the pace of job losses has reached its pace on faster since January 2013 ".

The 12-month outlook for these leaders remained "gloomy" on "lingering concerns about trade disputes, the slowdown in the auto sector and Brexit".

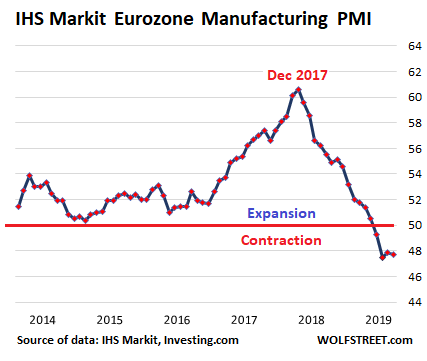

Eurozone

The IHS PMI Markit Eurozone Manufacturing further declined to 47.7 in May (after 47.9 in April), the fourth consecutive month of contraction and the lowest level in six years. .

But as in Germany, manufacturers of consumer goods continue to grow while manufacturers of intermediate goods and investment are in contraction:

- In the consumer goods sector, "growth has been maintained to a moderate degree" and has been in expansion mode for five and a half years.

- But the "marked" deterioration was "focused on the intermediate goods and capital goods sectors".

In the case of euro-zone countries, some are showing strength in the manufacturing sector. The weakest are Austria and Germany. Note which country has the fastest growing manufacturing sector in the euro zone:

- Greece: 54.5 (lowest in three months)

- Netherlands: 52.2 (two-month high)

- France: 50.6 (three months high)

- Spain: 2 (lowest in three months)

- Italy: 49.5 (eight months high)

- Austria: 47.8 (lowest since 50 months)

- Germany: 44.3 (two months low)

The weakness of manufacturing continues to be "closely linked to the deterioration of order books. The latest data show an eighth consecutive monthly decline in the number of new jobs received, "both domestic and foreign customers", "as shown by another sharp contraction" of new orders to export.

A fourth consecutive monthly decline in production and a further sharp drop in new orders has highlighted the fact that the sector remains the hardest in its history since 2013. Companies are tightening their belts, cutting spending and hiring. Input purchases, inventories and employment are all down, with manufacturers fearing to be exposed to a further decline in demand.

The most commonly cited risks were "trade wars, falling demand in the automotive sector, Brexit and wider geopolitical uncertainty" and they all "have the potential to hinder a stabilization of the manufacturing sector. ".

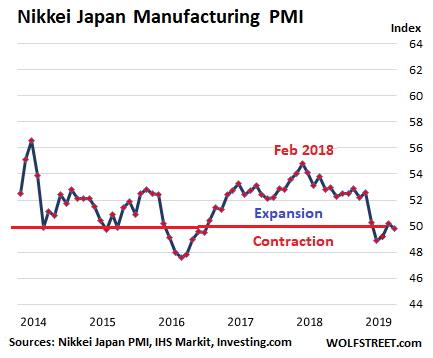

Japan

The manufacturing PMI Nikkei Japan Manufacturing rose slightly from 50.2 in April to 49.8 in May:

Employment rose, but at the slowest pace in two and a half years.

New orders fell for the fifth consecutive month, "a reflection of weakness both at home and abroad". Export activities declined for the sixth consecutive month, "which companies attributed to the difficult economic conditions of key trading partners such as China. as well as increased competition at the international level. "

As the appetite for Japanese products dwindled, companies reduced their inventory levels and reduced their buying activity. Inventories of finished goods and inputs decreased in May.

After showing signs of a slight rebound in April, future output forecasts became pessimistic in May for the first time since November 2012, as concern over increased trade tensions between the United States and China and the expected rise in sales tax later this year.

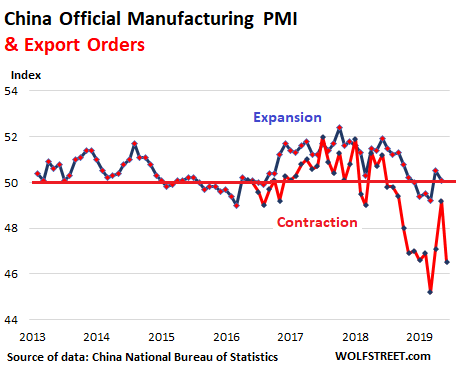

China's official and private PMI

The official Chinese manufacturing PMI, published by the National Bureau of Statistics of China, returned in contraction mode in May (49.4%), after two months of development. The sharp decline over several months in export orders (red line with data dating back to 2016) is particularly important:

Some hors concours:

- The production index continued to expand (51.7) but at a slow pace.

- New orders fell slightly (49.8%), driven by new orders for export (46.5%).

- Purchasing volume index up (50.5)

- The contraction in the index of imports has increased even more (47.1 in April compared with 49.7 in April).

- Employment index down sharply (47.0), in contraction mode since at least mid-2017

- The leaders remain optimistic, however, with an index of production and activity estimated at 54.5.

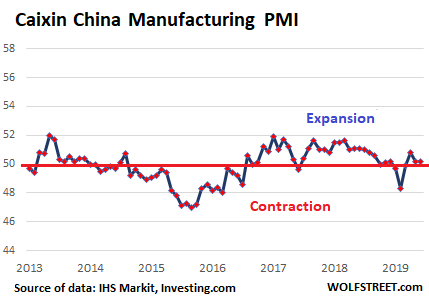

A slightly more optimistic version comes from the private sector Caixin China General Manufacturing PMI, which is barely in expansion mode for the third consecutive month:

"Chinese manufacturing companies reported a slight further improvement in general operating conditions in May," the report said. "The total number of new jobs grew faster, thanks to a further increase in export sales, while production was generally stable."

- The backlog of work continued to increase.

- There was "a further increase in the total number of new orders". It was "supported by a further increase in export sales. According to panelists, new product launches and stronger foreign demand have supported expansion. "

- But there was a "slight decline" for the second month in a row.

- Business confidence fell "to the lowest level since the series began in April 2012," citing "concerns over the intensification of the Sino-US trade war and forecasts of global demand relatively moderate ".

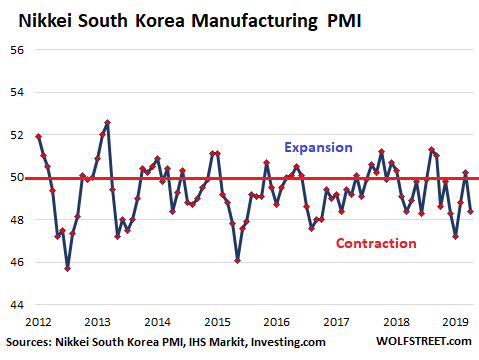

South Korea

The South Korean manufacturing sector is much smaller than the big four: China, the United States, Germany and Japan. But it's the next biggest line. And these leaders are a rather negative group, indicating that the manufacturing sector has been in decline for most of the time since 2012, according to the Nikkei Manufacturing PMI in South Korea, which had fallen into contraction mode in May (48.4). :

"Production has been reduced, with demand becoming increasingly difficult as domestic and export markets remain fragile," the report says. Some hors concours:

- The "faster decline in new orders" was attributed to "the fragility of the situation both in the domestic market and in the main export markets. New export orders declined for the tenth consecutive month, and the decline accelerated.

- Sales were affected by "the slowdown in automotive and semiconductor-related industries."

- Panellists cited "difficult trade with foreign customers in Japan, China and other parts of Asia".

- Production was contracted in May, as a result of lower orders.

- The numbers were reduced for the sixth month in seven months. "According to panelists, the reduced workload has led some workers to resign voluntarily."

- Arrears decreased for the ninth consecutive month.

Compared with the difficulties in the large German, Chinese, Japanese and South Korean manufacturing plants, all of which are export-oriented, the US manufacturing sector is still the cleanest dirty blouse – expanding, but with a slowdown of growth.

The economy is in a "very good situation," says Trump's man at the Fed. And the Fed's favorite measure of inflation is rising. Lily... US consumers support the economy. Wall Street calls for multiple rate cuts. The Fed stands out from Wall Street

Do you like to read WOLF STREET and want to support it? Using ad blockers – I fully understand why – but you want to support the site? You can give "beer money". I like it a lot. Click on the beer mug to find out how:

Would you like to be informed by email of the publication of a new article by WOLF STREET? Register here.

[ad_2]

Source link