[ad_1]

General Electric (GE) and its investors do not seem to be able to pause these days. Despite the upcoming changes to the company, which will involve a complete restructuring of its business by removing what is considered essentially non-core business, investor confidence continues to break. Just when the conglomerate can focus on execution and rebuilding shareholder confidence, another decline is due to decommissioning. JPMorgan Chase (JPM). Although I'm generally optimistic about the company, JPMorgan is still right in thinking that there are still problems in the business, including the one I've been thinking about for a while and the direction should solve.

A big problem or a small problem?

A few weeks ago, according to an article, Exelon Corp. (EXC) has discovered a problem with just one of its HA turbines in a Texas plant. In response to this problem, the company eventually shut down this turbine and, to be safe, it decided to close three more units. Although a handful of turbines may not seem significant, the fact is that they are. Take, for example, three turbines of the same class located in Pakistan. According to General Electric, these three units alone provide enough power to meet the needs of 7.3 million homes. In short, these are not small things.

Since Exelon's decision to close the turbines, General Electric has investigated the problem and, following an examination, they announced that a problem of oxidation related to one-piece turbines had caused failure of the first stage blade. The fact that management has described this as a minor problem would be reassuring for investors if credibility at the top has not been questioned so accurately in recent years, but if the problem is related to a single component, the patch arrives quickly.

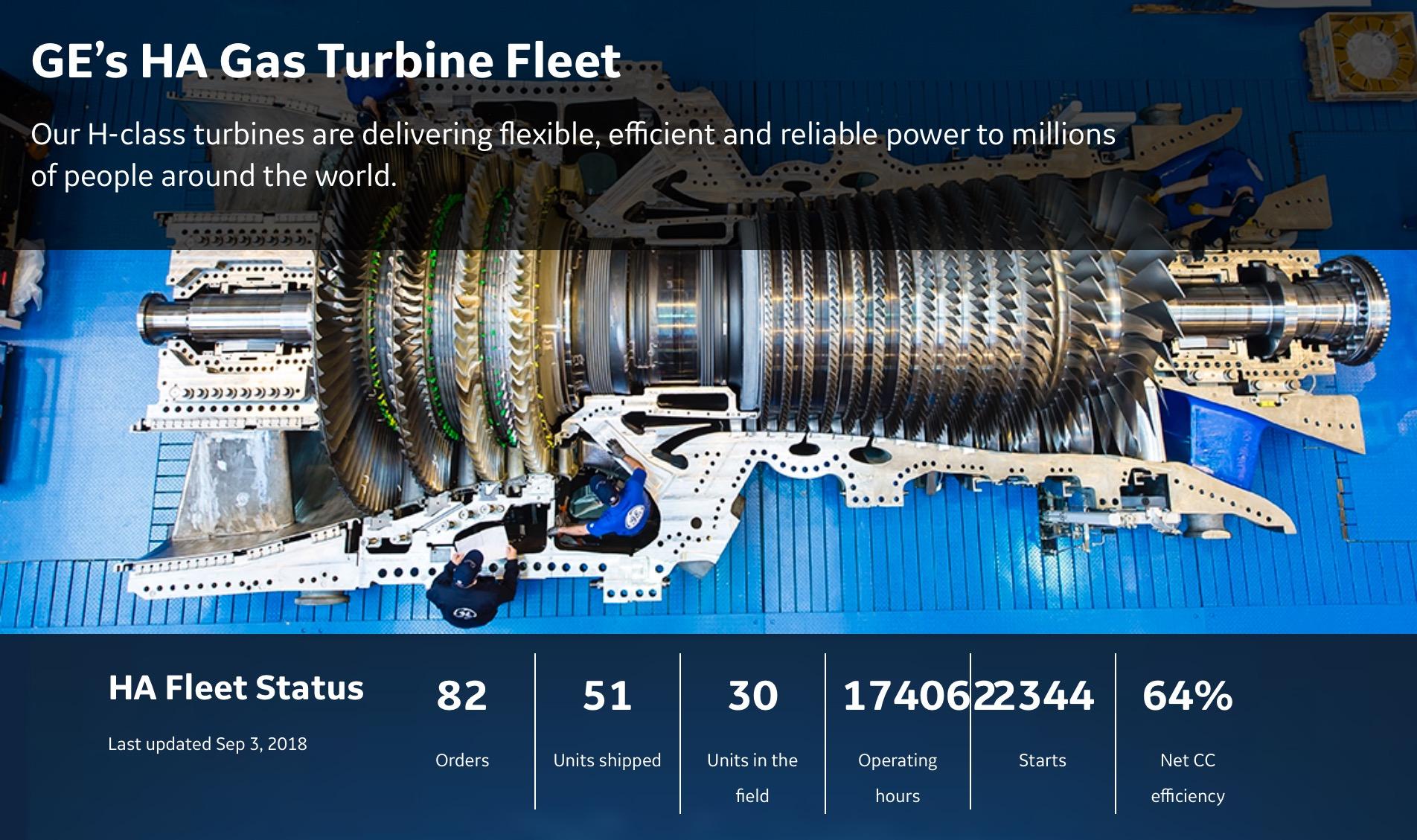

* Taken from General Electric

Unfortunately, the problem does not stop with the four Exelon units. Management must apply the same patch preventively to all shipped units. As you can see in the image above, as of September 3 of this year, of the 82 orders received by General Electric, this one has only 30 on the ground, but it has shipped 51 units. Each of these units will need to be repaired, but in addition to the troublesome part of the turbines, management says they are working as intended and that long-term performance issues should not exist.

A look at the HA gas turbine

More likely than unlikely, this problem, even though it only requires a small correction, will cost several million dollars to General Electric. That is why, in response to this news, JPMorgan announced that it was reducing its expectations for General Electric, not only for this year, but also for the next one. While keeping the same things, they expect the business to generate earnings per share of $ 0.75 this year (fiscal year 2019), down from the prior guidance of 0.80. $ per share. To put it in perspective, Wall Street estimates demand $ 1.04 per share this year, while General Electric itself said earnings should be between $ 1 and $ 1.07 per share. Next year, JPMorgan's forecast predicts that the conglomerate will generate earnings per share of about $ 0.82, compared to $ 0.92 per share previously anticipated.

While a review for this year should be necessary, I find it difficult to see this continue in the next fiscal year. Indeed, it is essentially a one-off event, such as when car manufacturers have to issue reminders for a defective part. That's why, despite the downward revision of earnings and the $ 11 per share downgrade to $ 10 that JPMorgan has set as its target price, I have a hard time seeing how this new could be to it. only bear fruit. a market value of $ 3.48 billion and how, based on the $ 1 revision of JPMorgan's target price, it could justify a total adjustment of the conglomerate's value of $ 8.69 billion.

One argument could be that this development could scare away potential customers, but it's hard to believe because the fact is that General Electric has the best new units in the market. You see, by 2030, management expects to have 500 HA turbines in the market, but that 's because of one thing: performance. At the beginning of the year, for example, the management revealed that in recent months, its class H turbines have beaten not one, but two world records. One of them was the highest efficiency rate ever achieved in a 50 Hz plant (62.22% efficiency), while the other was the highest efficiency ever achieved in a plant. a 60 Hz plant (63.08% efficiency).

If all goes as planned, management is confident that it will be able to achieve a 64% return on its turbines by 2020, but the company's main goal is to reach 65%. At first glance, it may seem that small changes like these are not significant, but the truth is far from it. Going back to the example of Pakistan's fuel-importing country, General Electric said every percentage point of efficiency improvement could reduce fuel savings by $ 10 million out of 10 years for a 1,000 MW plant.

Given these world records, it is undeniable that General Electric has the best new unit on the market and that is why customers will continue to buy them despite this "minor" performance problem. That said, it does not change my opinion on the company's Power segment, where the HA gas turbines are hosted. according to UBS Group AG (UBS), about 20 years ago, the conglomerate controlled nearly half of the global market share of turbines. Today, this figure is closer to 11%. While the strong performance of these units will help the company, it is also important to keep in mind that GW's demand for production capacity is expected to decrease this year compared to the past year and is expected to decline further. the next year. the picture will not be easy for any player in the space.

To take away

It seems to me that, given all that is happening with General Electric's HA gas turbines, JPMorgan was right to revise its profits down for at least this year, but to expect a problem sustainable is an overreaction. According to management, the solution to his current problem seems rather simple and easy. If this is true, the market is only hitting General Electric not for fundamental reasons, but because the market is becoming suspicious of management. is not bullish. In the end, fundamentals must always decide the outcome of any investment, but for a company as unappreciated as General Electric, short-term news can be painful.

Great announcement!

In early October, I will be launching my own Marketplace service here. Its purpose will be to provide detailed analyzes of the cash flows of oil and gas producers, and then to perform both an absolute and a relative valuation for the companies in question. I already have 20 companies to include in this service, but in the coming months, my goal is to raise it to at least 50, collectively with a market capitalization of over $ 500 billion. More details coming soon!

Disclosure: I / we have no position in the actions mentioned and we do not plan to enter positions in the next 72 hours.

I have written this article myself and it expresses my own opinions. I do not receive compensation for this (other than Seeking Alpha). I have no business relationship with a company whose stock is mentioned in this article.

[ad_2]

Source link