[ad_1]

Source: TheVerge.com

Nvidia: another star falls

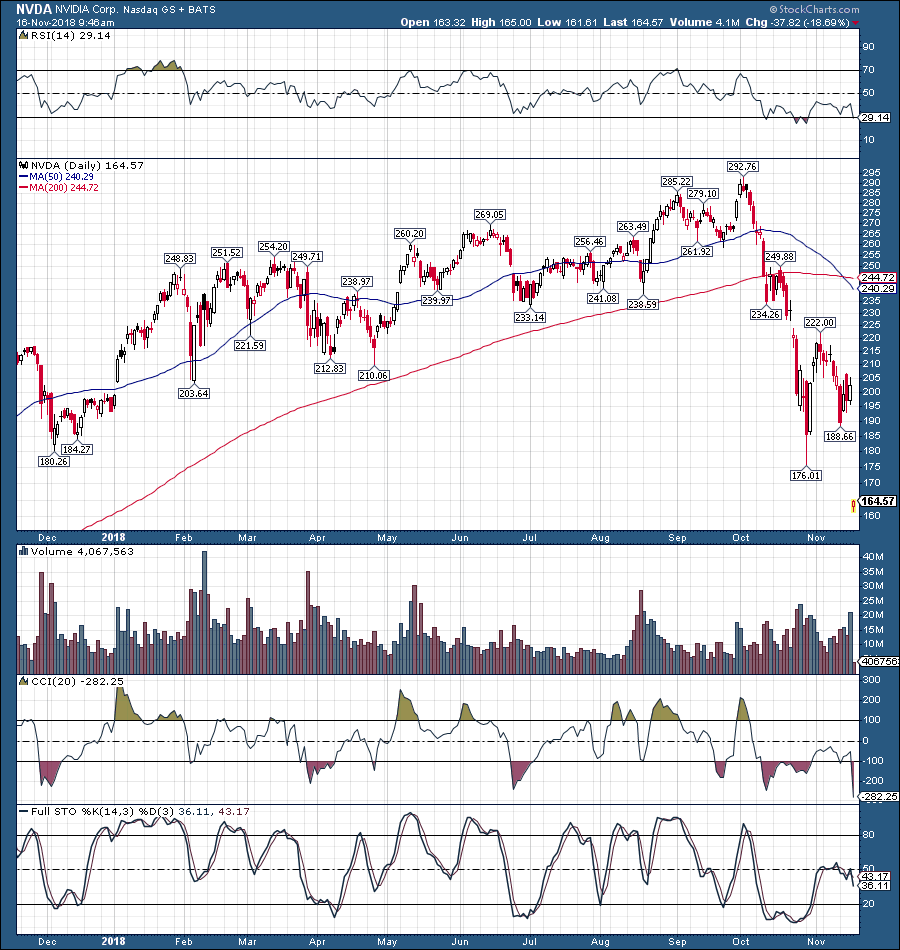

Nvidia (NVDA) has collapsed nearly 20% as a result of the latest earnings announcement, bringing the company's total decline from its all-time high to around 45% in just six weeks. A rotation of multiple inventories and high technology names coupled with depressing earnings and forward-looking forecasts has helped bring Nvidia's stock to levels not seen for more than a year.

NVDA 1 year chart

Source: StockCharts.com

So, is this a gold buying opportunity to own an incredible company whose valuation is greatly reduced, or is it a sign that further declines are likely to materialize both in Nvidia and in other prestigious names?

More than a correction now

When leading industry names, such as Nvidia, fall by more than 40% in a few weeks, this is more of a correction. Bear or not, one thing seems clear, these types of movements are not indicative of a healthy market.

The most disturbing is perhaps the fact that Nvidia is not the only one. Other names of major growth countries have recorded similar craters in recent weeks and months. Facebook (FB) decreased by 36%, Amazon (AMZN) by 28%, Netflix (NFLX) by 36% and even Google / Alphabet (GOOG) (22%). Technically speaking, all FANGs are in bear market territory, some deeper than others.

However, the sharp declines go far beyond the FANGs, even the mighty Apple (AAPL) has recently lost more than 20%. In fact, nearly half of the S & P 500 companies are now in bearish territory.

Source: AdvisorHub.com

Nvidia is another shooting star, among many others, and its decline also reflects the deterioration of the economic atmosphere surrounding actions in general. Low prices on Nvidia, as well as other names with high growth and high profile, suggest that revenue and EPS growth could continue to weaken and that equities could continue to fall as a result. .

Nvidia revenue report

- EPS was $ 1.84 against an estimate of $ 1.71.

- Revenues were $ 3.18 billion versus $ 3.24 billion, with missing estimates of $ 60 million.

- Futures forecasts rose to $ 2.7 billion from $ 3.4 billion, representing a huge loss of more than 20%.

- Gaming revenue was $ 1.76 billion, up from $ 1.89 billion.

- Data revenues were $ 792 million, compared to $ 821 million.

- Visualization sales were $ 305 million versus $ 284 million.

Nvidia may be a great company, but its results are largely horrendous. The slight EPS beat is largely irrelevant, as Nvidia is considered a high-growth, multi-digit name. The relatively large shortfall, combined with the much lower-than-expected forward-looking forecasts, suggests that the slowdown in Nvidia's business is much larger than expected. In addition, this further suggests that a broader economic downturn is likely preparing.

A 20% loss in revenue forecasts is a staggering disappointment from the point of view of growth. That means that instead of providing the expected growth of 13.2% in business revenue next year, the company could generate only a very small, if any, growth in the business. business figure next year. In fact, the lowest income estimates indicate stable growth year-over-year. This would also imply that the company's EPS could be stable or even decline on an annual basis.

Analysts seem too optimistic about Nvidia

It's not always a good thing that everyone seems very optimistic for a company. In fact, this can sometimes be a meter indicator. After all, when everyone is already optimistic, there are fewer market participants to convert to the bullish camp to create an additional buying interest. On the contrary, when the tide turns, many market players may change their minds, sell the shares or even reduce the company's shares.

It is remarkable how optimistic analysts are about Nvidia, both remarkable and disturbing. Of the 26 equity analysts, 15 have good buy ratings, four buy ratings and seven stock hold ratings. Of course, there are no sales recommendations on Nvidia.

However, the shocking factor lies in the price targets set by analysts on Nvidia – the 12-month price targets range from $ 225 to $ 400, with a price target of $ 300. This indicates that, compared to current prices, Nvidia is expected to gain about 33% over the next year just to reach the lowest end price targets. The stock should then appreciate about 80% to reach its consensus price target and 140% to reach its final price target of $ 400 higher.

What is the price Nvidia, really?

It is great that analysts are so optimistic about the prospects of the title Nvidia, but to what valuation is this title considered overvalued? Nvidia is expected to earn $ 7.30 this year and $ 7.95 next year (fiscal year 2020). This means that now, with $ 170 per share, Nvidia is trading at about 21.4 times the projected earnings of next year. This is not particularly cheap, especially since the growth of BPA should be only 8% YoY and revenue growth is expected to slow to 13 percent year-over-year.

In addition, given the recent revenue losses and extreme poverty forecasts, revenue growth could only increase by 1% next year, and profitability should also fall. Essentially, EPS could be stable or even decline year-over-year, so the direct multiple is probably much higher than the one announced.

However, even if we apply the unrevised earnings estimates to analysts 'price targets, we begin to find that analysts' price forecasts seem extremely optimistic. With a price target set at $ 300 per consensus, Nvidia trades at a P / E multiple of about 38, and at $ 400 the company would have a P / E multiple of 50. This is astronomically high for a company faced with a significant slowdown leveling the EPS.

In addition, the company is already trading about 10 times its sales, which is quite high, at $ 300, it would be about 15 times the sales and at $ 400, Nvidia would be a $ 250 billion company trading at 20 times. These assessments seem extremely high, unrealistic even to some extent.

If we use a price / earnings growth approach, Nvidia is trading at a PEG ratio of 2.66 based on next year's forecast, which is also quite expensive. Basically, no matter how you look at Nvidia, even with its current "up-to-date" valuation, the stock is far from cheap at the moment. This is particularly true given the slower nature of the growth of the current economic environment in which Nvidia is located.

Therefore, and despite the extremely optimistic view of analysts on Nvidia, the stock is most likely to trade mainly laterally to reach a price below $ 300 – $ 400 soon. These price targets could perhaps be achieved within a few years (3-5), but 12 months seems extremely unlikely. In fact, I expect Nvidia to trade at roughly current levels or maybe even a year from now.

The Bottom Line: It goes well beyond Nvidia

Nvidia is just another fallen star among many well-known names, which have experienced weaknesses in recent months and quarters. Many growing companies, including Amazon, Alphabet, Facebook, Apple, now Nvidia, and many others have announced lower-than-expected revenue and / or disappointing forecasts.

This probably implies that a broader economic downturn is preparing or even a recession. It also suggests that downward revisions in profits and revenues should be realized for many companies.

As a result, valuations, multiples and share prices may continue to contract over the next few quarters. This is not just about Nvidia and other high-growth multiple stocks, but also shares in general.

Nvidia has been severely punished in recent weeks. Relief is therefore possible. However, I would like to take advantage of this upcoming opportunity to lighten the positions as it is unlikely that this stock will appreciate significantly or reach new record highs so soon. In fact, in my opinion, the risks of additional weakness in the medium term are greater than substantial gains.

Thank you for taking the time to read my article. If you liked reading my work, please click on "As"button, and if you want to be informed of my future ideas, click on it"To follow"link.

Warning: This article expresses only my opinions, is produced for informational purposes only, and in no way constitutes a recommendation to buy or sell securities. The investment carries a significant risk of loss of capital. Please do your own research, consult a professional and review your investment decisions with the utmost care before jeopardizing your capital.

Want more? Want to complete articles which include technical analysis, trade triggers, trading strategies, portfolio overview, option ideas, price targets and more? To find out how to best position yourself for a rally in Nvidia, please register. Albright Investment Group.

- Subscribe now and get the best of both worlds: an in-depth view of values combined with successful growth strategies.

- Enjoy access to AIG's best-performing portfolio, which has outperformed the S & P 500 by 40% over the past year.

- Enjoy the limited time 2 weeks free trial offer now and receive reduction of 20 your launch subscription price. Click here to learn more.

Disclosure: I am / we have long been AAPL, GOOG, FB, NFLX.

I have written this article myself and it expresses my own opinions. I do not receive compensation for this (other than Seeking Alpha). I do not have any business relationship with a company whose actions are mentioned in this article.

[ad_2]

Source link