[ad_1]

September 24 was a dark day for shareholdersF Sirius XM (SIRI). After management announced its intention to acquire approximately 85% of Pandora Media (P) that does not already belong to him, investor confidence has caused a market value drop of $ 3.23 billion. Although the Sirius XM management team views the transaction clearly, the shareholders are naturally distraught. After all, while management is right about the benefits of the "everything in stock" operation, the fact is that Sirius XM seems to be paying too much for a low-quality company with limited long-term potential.

A look at the deal

For several years, Sirius XM has earned the reputation of being a powerful cash flow generator, but despite this, the company does not use its cash to pay Pandora. Instead, the company decided to issue shares to Pandora shareholders. In exchange for 1 Pandora share held by investors, Sirius XM will give 1.44 shares. Given the $ 6.98 share price that Sirius XM was trading on before the announcement of the transaction, this involved a price of $ 10.05 per unit for Pandora, a premium of 10.6% over at the previous closing.

Taking into account the net debt, the total purchase of Sirius XM from Pandora is expected to cost shareholders about $ 3.5 billion, but immediately after the announcement, Sirius XM shares fell by 10.3%. Even after Pandora dropped 1.2% in response to the announcement, the deal as it stands does not imply any significant premium for investors who decide to buy Pandora now. This is interesting because it suggests that the market considers it almost a concluded deal, although there is an explicit provision that would allow Pandora to seek a better deal.

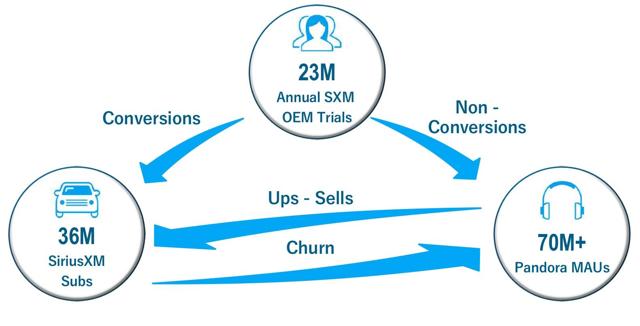

At the heart of the agreement, Sirius XM expects one important thing: the ability to use Pandora's large audience to create revenue opportunities and, possibly, other synergies, to enhance its own business. You see, while Sirius XM is a major player in the cross section of music and technology, with approximately 36 million subscribers and 23 million additional test listeners, Pandora, which currently has more than 71 million active users per month.

* Taken from Pandora Media

As you can see in the picture above, the management clearly sees this as a pipeline opportunity. Right now, Sirius XM's annual testing is converting (they're asking for a 40% conversion rate) or they're not doing it, and that's pretty much the end of the story. By controlling Pandora, Sirius XM can continue to offer its radio users the ability to listen to music and other content, while generating advertising revenue. Those who go out can return to Pandora while management wants to win them back in the future.

It's a tough business

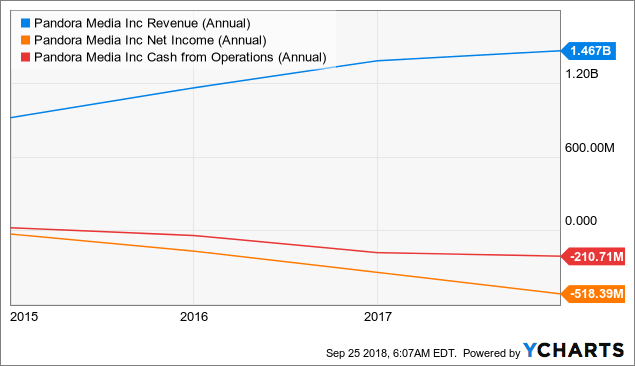

This kind of transaction, especially because of the network effects and the manufactured vertical integration it generates, is the type of transaction that I should normally consume. That said, the case of Pandora is different for one essential reason: the balance sheet of the company, because of its economic model, is terrible. Take a look, for example, at the graph below, which covers Pandora's revenues, net income and cash flow from 2014 to 2017.

P Sales (annual) by YCharts

Over this four-year period, Pandora's sales grew well, from $ 920.80 million in 2014 to $ 1.47 billion last year. However, the same can not be said of its results. In fact, the opposite is true. During the same period, the Company's net loss increased from $ 30.41 million to $ 518.40 million. If it was not cash, which resulted in positive or at least neutral operating cash flow, I could understand, but it is not. Between 2014 and 2017, cash flow from operations increased from $ 21.03 million to $ 210.71 million.

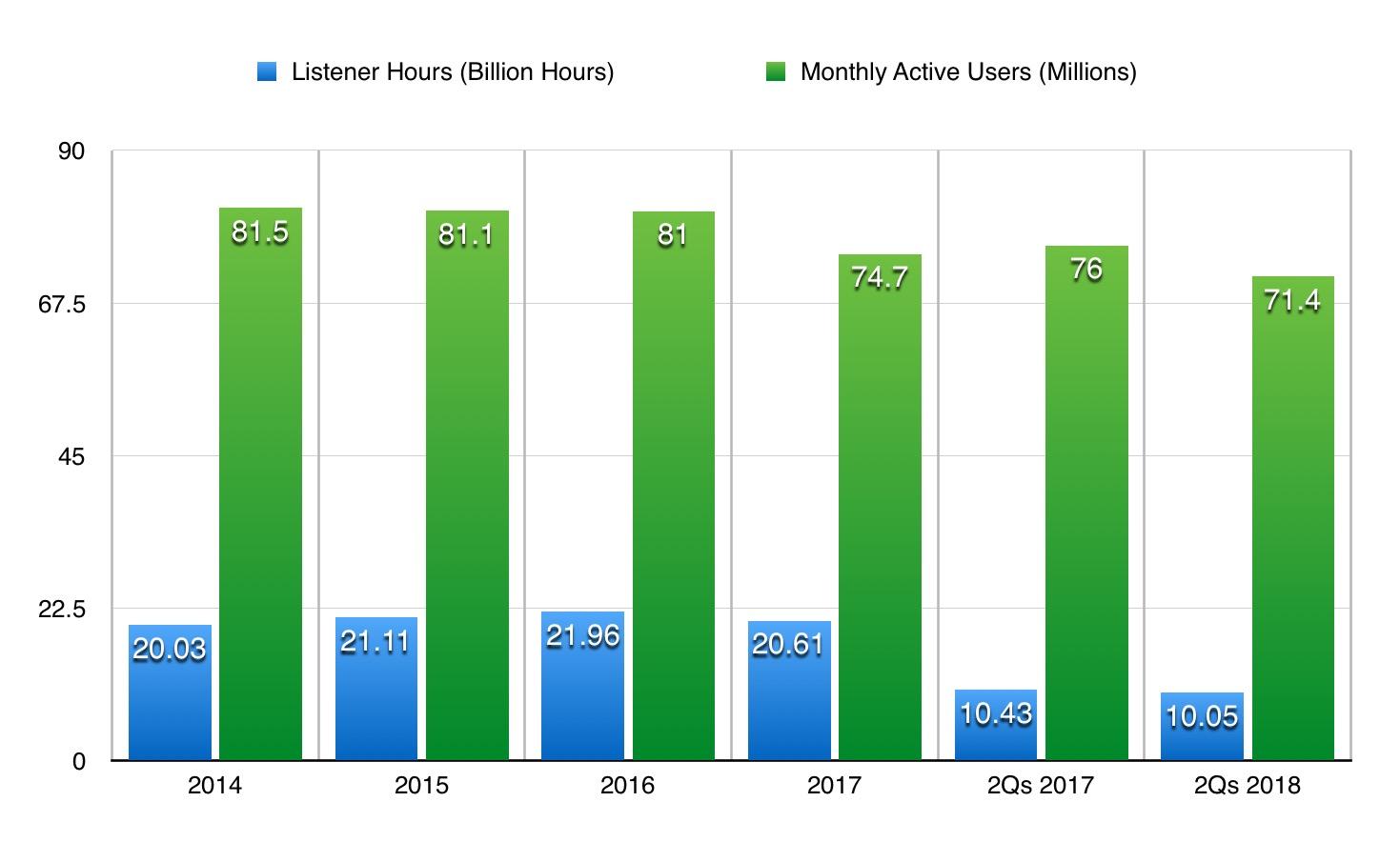

Robust growth is a legitimate way to rationalize both net losses and negative cash flows, but this has not been the case either. As you can see in the graph below, Pandora's listening times have increased from 20.03 billion hours in 2014 to 21.96 billion hours in 2016, but this figure dropped to 20.61 billion hours last year. In the first half of this year, auditor hours totaled 10.05 billion hours, up from 10.43 billion hours at the same time last year, which seems to be worsening. In the same graph, you can observe a rather disturbing trend: the number of active users decreases to a significant level.

* Created by the author

Between 2014 and 2017, this measure increased from 81.5 million to 74.7 million, but continued in 2018. According to management, in the second quarter of 2017, the number of active Pandora users was 76 million. Today, this figure is 71.4 million and it seems that the trend is downward. Some investors may rightly point out that paid subscribers on Pandora went from 4.39 million in 2016 to 5.48 million last year, but despite this and the incomes that accompanied it, the results financial problems have worsened.

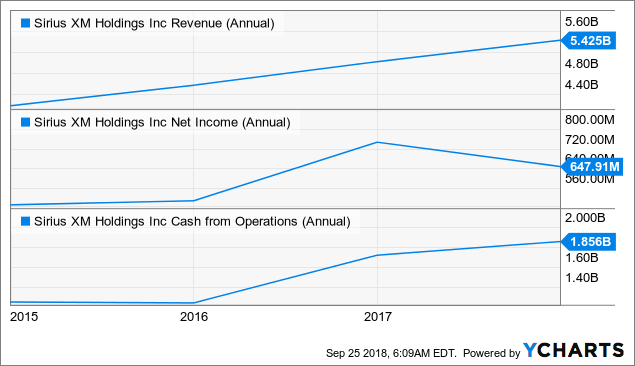

SIRI Revenue (Annual) data by YCharts

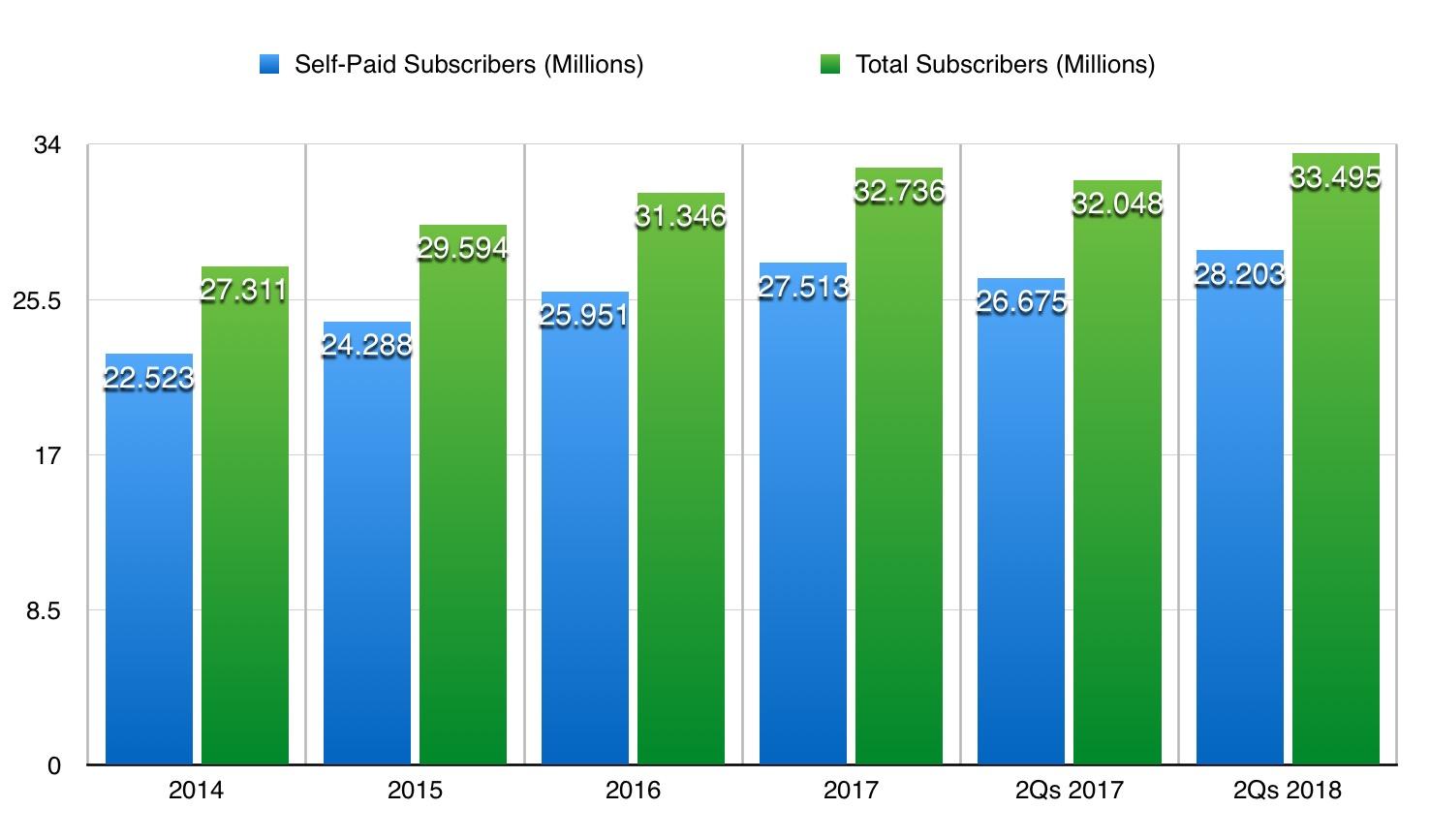

Now, let's look at Sirius XM. In recent years, the company also saw its revenue increase, but unlike Pandora, Sirius XM has consistently increased its operating cash flow with a good result and generated positive results. Not only that, but also unlike Pandora, it seems that there are no problems with the growth of its user base. As you can see in the graph below, you can see that the number of paid subscribers has increased from 22.52 million in 2014 to 27.51 million. This year, growth is expected to slow down a bit, but even with that, Sirius XM is expected to add 1.15 million self-paid net subscribers throughout 2018. Meanwhile, the total number of subscribers to this activity increased from 27.31 million in 2014 to 32.74 million last year. .

* Created by the author

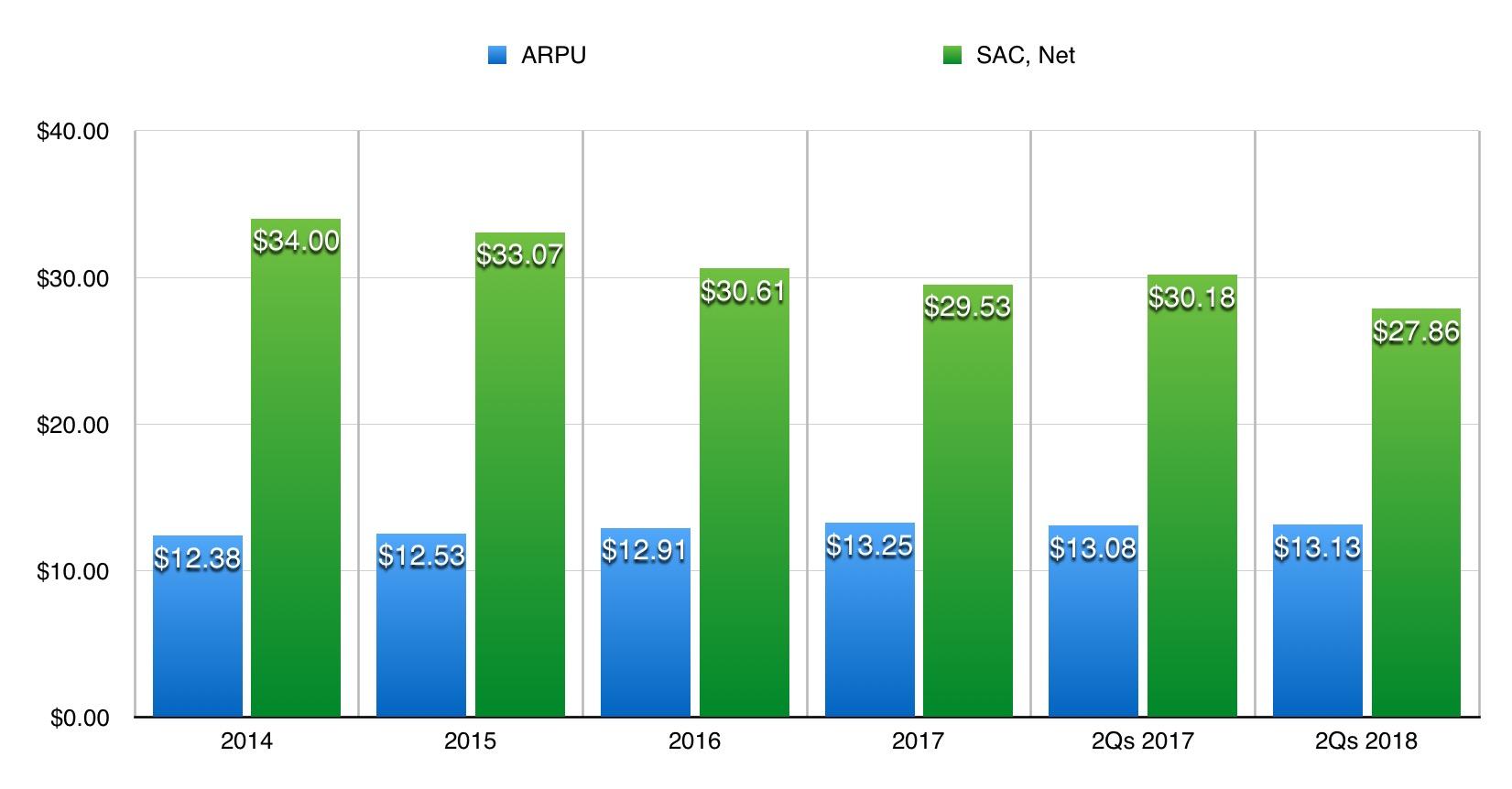

Not only was the growth positive, but the management also recorded further improvements in terms of revenues and costs. In 2014, the ARPU (average revenue per user) was $ 12.38 per month. Last year this figure had risen to $ 13.25 per month. Meanwhile, the net acquisition cost (SAC) of Sirius XM has dropped only. In 2014, this figure was about 34 dollars, but it has since fallen to 29.53 dollars. To put this in perspective, including the net debt absorbed, Sirius XM pays $ 49.02 for each of Pandora's monthly active users, and this is the case if the decreases cease.

* Created by the author

To take away

I am a big fan of synergistic network effects and it is possible, according to management, that Sirius XM shareholders can take advantage of the evolution of their customer portfolio, but I am afraid they will pay too much for Pandora. Yes, revenue is growing and the subscriber base is paying off, but the user base is decreasing, net losses and cash outflows are growing rapidly and the price paid by Sirius XM seems high considering estimated acquisition costs. I'm afraid it will take a lot of management effort for Sirius XM's common shareholders.

Disclosure: I / we have no position in the actions mentioned and we do not plan to enter positions in the next 72 hours.

I have written this article myself and it expresses my own opinions. I do not receive compensation for this (other than Seeking Alpha). I have no business relationship with a company whose stock is mentioned in this article.

[ad_2]

Source link