[ad_1]

Banks, as blue chip brokers and counterparties to the hedge fund, are eating multibillion dollar losses as they attempt to break out of these covert positions in equity derivatives.

By Wolf Richter for WOLF STREET:

The implosion of an undisclosed hedge fund, now widely reported as Archegos Capital Management, hits the stocks of the banks that served as the fund’s primary broker. Heavily leveraged, equity-based derivative positions had exploded dramatically. Banks engage in these risky leverage operations because they generate huge profits – until they explode and the banks are hit as counterparties.

Swiss credit [CS] is down 13% for now in trading in the US after warning this morning that “a major US-based hedge fund defaulted on margin calls made last week by Credit Suisse and certain other banks ”, and that he and“ a number of other banks are exiting these positions ”and that the loss resulting from this exit“ could be very large and significant to our first quarter results. The bank deemed it “premature to quantify” the loss.

Nomura Holdings [NMR] is down 14% for the time being in trading in the United States after warning this morning that “an event has arisen which could subject one of its American subsidiaries to a significant loss resulting from transactions with a United States customer.” He estimated the loss of this customer at “about $ 2 billion, based on market prices as of March 26”.

As Credit Suisse pointed out, “a number of other banks” are also involved as counterparties to this unnamed hedge fund, and have been trying to get out of those positions since last week.

Deutsche Bank came out of its positions unscathed, according to a spokesperson, quoted by the Wall Street Journal, perhaps because it was properly hedged: “We are managing the remaining intangible client positions, on which we do not expect to suffer any damage. loss, “he said.

Last week, Archegos – who manages the wealth of former Tiger Asia manager Bill Hwang and his family – received margin calls from these banks which forced her to liquidate her positions. Last week alone, not counting today’s liquidations, sales approached $ 30 billion, according to Wall Street Journal sources.

In a margin call, the broker, as a lender, requires the client to provide more collateral if the price of a leveraged position has fallen sharply. If the client fails to do so, the lender will sell the securities to recover the amount owed. But in this case, the sale of the collateral was not enough to cover what is owed, and the banks eat the losses.

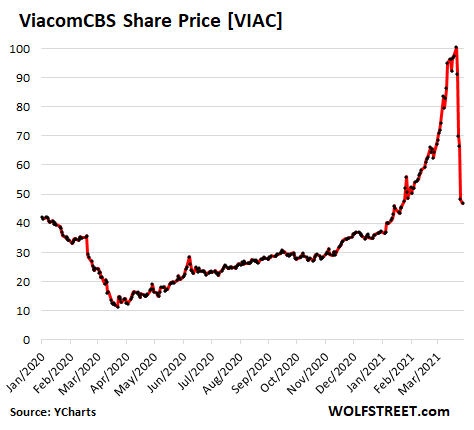

The American Depositary Receipts (ADRs) of Chinese companies, such as Baidu, GSX Techedu, Tencent Music, and shares of US media companies such as Discovery and ViacomCBS, were heavily involved in these liquidations. And their stocks, having skyrocketed since last March, have collapsed.

ViacomCBS [VIAC] collapsed 54% in five trading days, including today. But after the ridiculous surge – quadrupling between early August and March 22, and a 10-fold increase from the March 2020 low, amid general market mania – stocks are now back to where they were just two months ago. …

The forced liquidations became apparent last week with the sale of huge blocks of shares, including shares in Discovery and ViacomCBS, by Goldman Sachs, Deutsche Bank, Morgan Stanley and other banks, amid swirling rumors according to which a hedge fund had collapsed.

The positions “may have exceeded $ 50 billion,” but they were not real stocks, but equity-based derivatives, called Contracts for Difference (CFDs), and Archegos may not have never owned any of the underlying stocks, according to Bloomberg this morning, citing people familiar with the matter. The size of the fund remains uncertain, but before all of this happened it was estimated to have grown from $ 5 billion to $ 10 billion, taking these leveraged trades to the top.

It’s also unclear what’s left of the fund at this point, but one thing we already know: Some of the losses have been eaten up by the banks.

A CFD is a contract between the trader, like Archegos, and the broker like Credit Suisse, Nomura, Goldman Sachs, etc. It is a type of stock exchange. The leverage can be huge and the trading is opaque and does not involve any exchange, but takes place between the trader and the broker or a market maker or between parties. In the United States, CFDs are illegal for retail traders, but not for hedge funds.

The fact that Archegos’ positions are derivatives, rather than real stocks, has allowed it to take significant stakes – some of which give it more than 10% exposure to the shares of these companies – without having to disclose these issues to regulators, which it would have done. had to do with regular equity positions of this magnitude. This allowed Archegos’ exposure to these stocks to remain anonymous until transactions exploded.

The secretive nature of these transactions meant that the fund’s prime brokers, such as Credit Suisse, were unaware of the large-scale involvement of other blue-chip brokers, such as Nomura, Deutsche Bank and Goldman Sachs. And when they figured it out, it was too late. And last week, when the hard sell started, each prime broker was not alone in closing positions, but was doing it against other prime brokers trying to do the same.

This explosion is another sign of the leverage accumulated during this market mania and the exposure of investment banks to this leverage. How many hedge funds have yet to explode before the banks, in their role as prime brokers of these hedge funds, start singing the blues, while trying to get out of a myriad of positions?

The fact that the stock market leverage is huge – after a year of central bank money printing that shattered all previous records – has become clear with the only timely measure of stock market leverage we have, margin debt. It only covers a small portion of the overall stock market leverage, but it is reported monthly, unlike other forms of stock market leverage which are either not reported at all, or are reported on an ad hoc basis. by brokers in their annual reports, or are only reported when they explode.

And margin debt, ladies and gentlemen, has jumped historically, 50% from a year ago, most never, most ever. Read … Stock market leverage increases historically: another WTF chart of a zoo that has run out of nuts

Do you like reading WOLF STREET and want to support it? You use ad blockers – I fully understand why – but want to support the site? You can donate. I really appreciate it. Click on the mug of beer and iced tea to find out how:

Would you like to be notified by email when WOLF STREET publishes a new article? Register here.

![]()

[ad_2]

Source link