/cloudfront-us-east-2.images.arcpublishing.com/reuters/DDT66DJV7VJ7BDRBFKBY3PIH3U.jpg)

[ad_1]

Aug.26 (Reuters) – Federal Reserve Chairman Jerome Powell’s highly anticipated speech at the Jackson Hole economic conference on Friday is likely to offer little new clue as to when the US central bank may start cutting back on massive purchases of assets, analysts said.

But Powell could tackle the delicate task of explaining why cutting $ 120 billion in monthly treasury bill and mortgage-backed securities purchases does not mean looming interest rate hikes, making advancing an effort by Fed policymakers to keep traders from raising borrowing costs more than the central bank can feel justified or healthy for an economy with millions of unemployed.

“He will do his best to say that these are independent decisions… and that one doesn’t necessarily speed up the other,” said Steve Kelly, professor at the Yale School of Management. “That’s the biggest challenge … this communication around the rate cuts and increases.”

Fed officials agree.

The minutes of their July 27-28 political meeting show that many thought it would be important to stress that there is no “mechanical link” between the reduction in bond purchases and the rate hikes. .

Rejecting this link will not be easy. Many Fed officials also felt it would be best to end the bond buying program before raising rates. And they continue to debate whether to cut back on purchases quickly or lengthen them, for perhaps up to eight months.

Additionally, some policymakers argue that bond purchases don’t help much anyway, as they are aimed at boosting demand but cannot resolve the bottlenecks companies face as they struggle to win. meet this demand as the economy quickly reopens.

With so much instability, the odds were always great that Powell would use his remarks at the Kansas City Fed Central Bank Conference, which normally takes place in Jackson Hole, Wyoming, but is held for virtually the second year in a row, to satisfy investors. want details on the tapered timeline.

This is especially true now, as the burgeoning Delta variant of the coronavirus shows signs of slowing economic recovery in the United States, especially in areas of the country hardest hit by infections. read more The data raises new questions about what appeared to be an internal consensus emerging when the Fed met last month to begin withdrawing its extraordinary support for the economy later this year.

Even the Dallas-based Fed Kaplan, one of the central bank’s biggest supporters of an early withdrawal, said last week that it was starting to see signs of Delta’s impact and would keep the open minded ahead of the Fed policy meeting next month. Read more

“It’s hard to imagine the Fed committing to a specific timeframe in light of the ongoing public health crisis,” Jefferies economist Aneta Markowska said of Powell’s upcoming speech.

Powell, who is due to speak by webcast at 10:00 a.m. EDT (2:00 p.m. GMT) Friday, could acknowledge the economy’s progress towards full employment, Markowska and other economists said. While Powell wants to keep the door open when the reduction starts in November, he will be “very cautious” about locking in such a timeline, Goldman Sachs economists said in a note this week.

COMPLICATED MESSAGING

Economists polled by Reuters expect the US economy to create an additional 725,000 jobs this month, on top of the nearly 1.9 million gained in June and July. And inflation – a new reading of which will be released shortly before Powell’s speech – has been above the Fed’s 2% target for months, though most U.S. central bank policymakers expect it to be. ‘she moderates later this year.

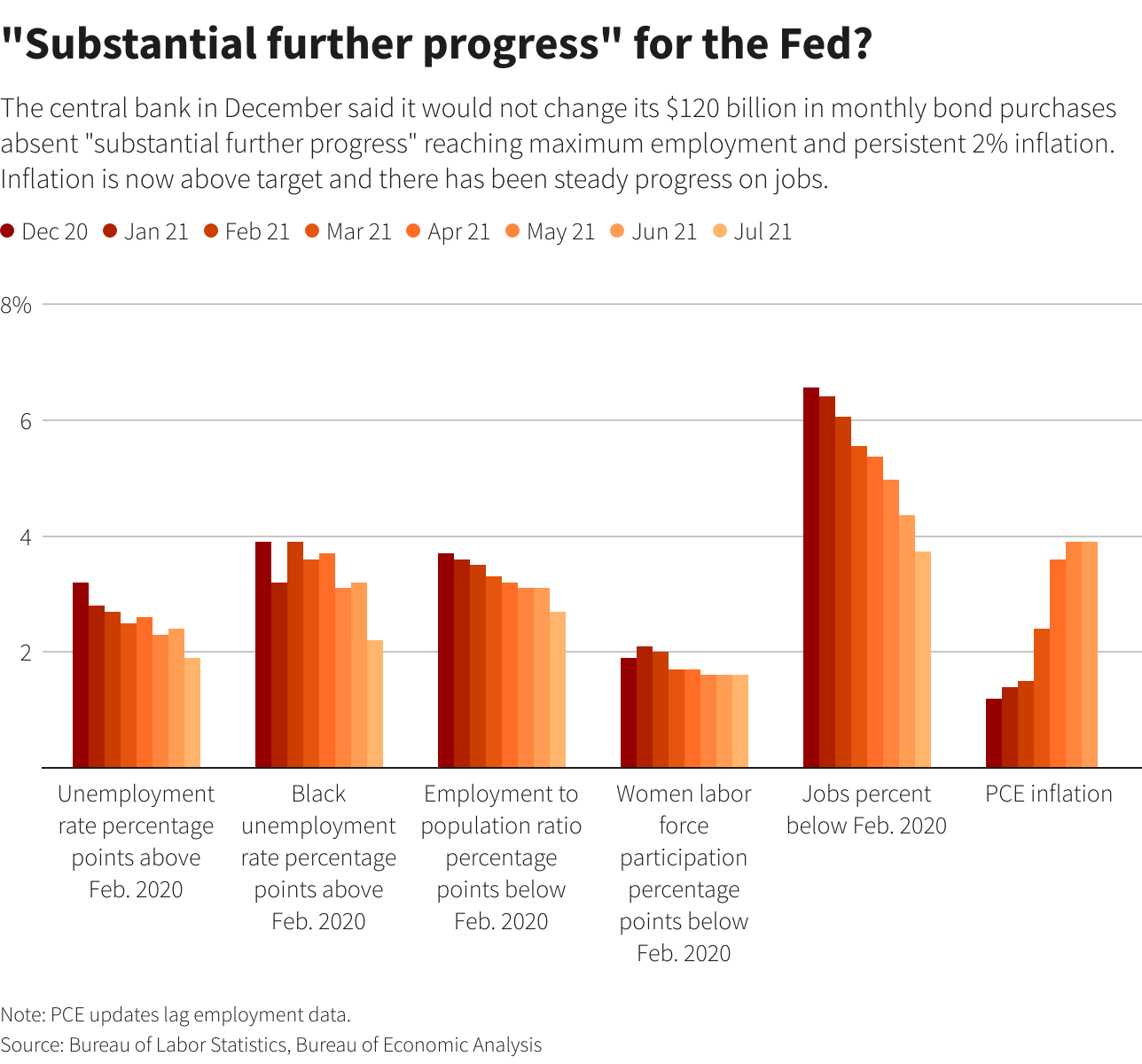

Data suggests to many Fed policymakers that the economy is on the verge of making “further substantial progress” towards full employment and 2% inflation, the bar they set before agreeing to cut monthly asset purchases.

But to keep long-term interest rates low for an economy that is still recovering from the pandemic-triggered downdraft, Powell will also want to point out that the hurdle to reducing is nowhere near the three-part trigger for the hikes. rate. The bar for increasing borrowing costs is actually reaching full employment and seeing inflation on track to be moderately above 2% for a while.

“It’s a complicated message right now,” said Tim Duy, chief US economist at SGH Macro Advisors. “The reality is that tapering is not separate from rising rates: once you start tapering, you kind of start a clock on rising rates.”

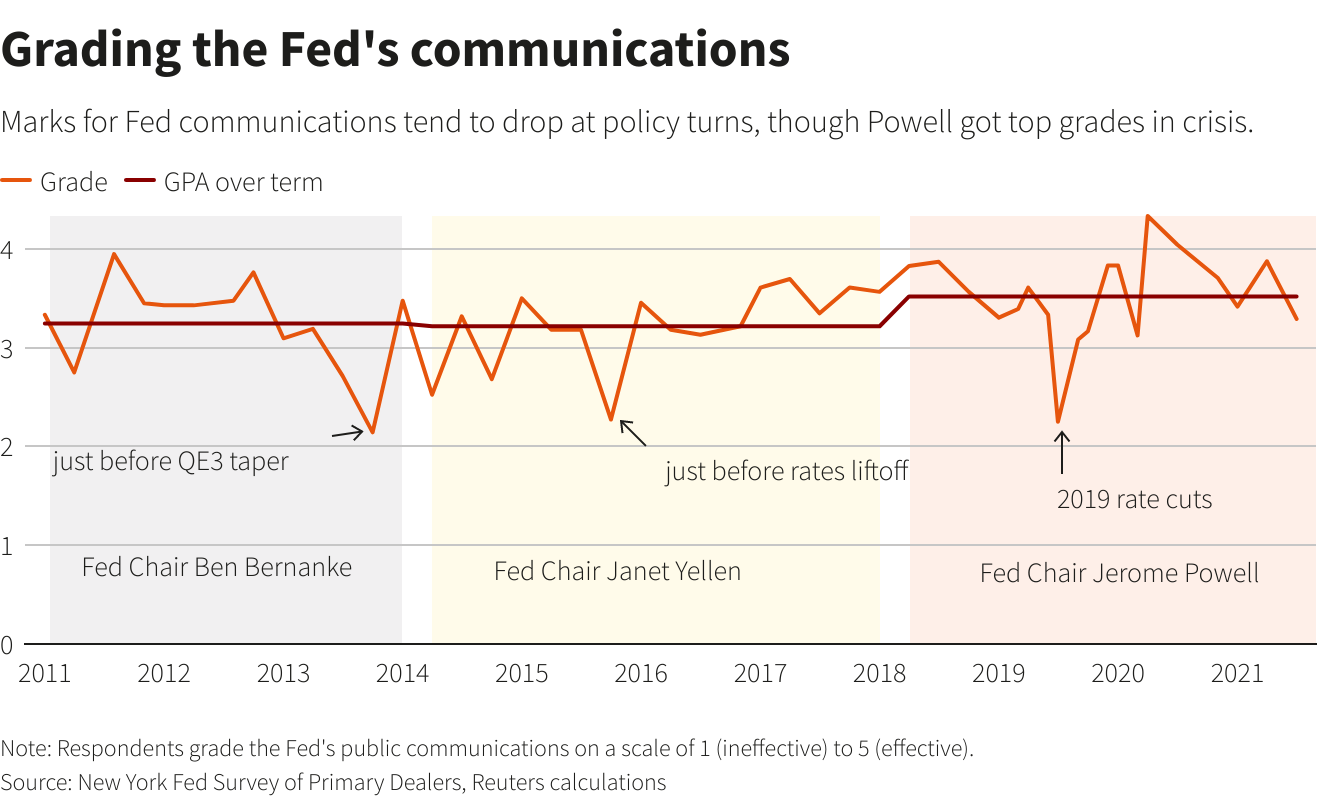

And yet, it is this kind of quick reaction that Powell will want to avoid. In 2013, when then Fed Chairman Ben Bernanke attempted to gently foreshadow an upcoming cut in bond purchases, traders responded by raising long-term rates so sharply that the Fed eventually had to delay reducing its purchases.

The markets generally judge the Fed’s communications more harshly at such political turning points. If they do it again, it could prove to be awkward timing for Powell, as US President Joe Biden is debating whether to appoint him for another four years as Fed chief.

Despite the deterioration in Wall Street ratings, it is clear that the Powell-led Fed is on the verge of declining, although his speech this week should offer little news on exactly when.

Even the accommodating San Francisco Fed chairwoman Mary Daly said last week that she was confident the economy would meet the bar the central bank has set to start cutting support by the end. of this year.

“The key message here is that it’s time to really think about reducing the level of support we give to the economy because the economy is truly self-sufficient,” Daly said in a virtual interview with Barron’s Roundtable, adding, however, that she would be “open-minded” about the impact of the Delta variant and could see a delay until next year.

Reporting by Ann Saphir Editing by Paul Simao

Our Standards: The Thomson Reuters Trust Principles.

[ad_2]

Source link