If you want to mention a keyword that gives you a migration bank, I think it's an "immediate annuity." If the question is very simple, the financial authorities are asking the insurer to "pay the money" to consumers in the form of a "lump sum payment," and the insurance company has of a map "general relief" without legal basis, It can be summarized as a situation that is repulsed like a whirlwind. But there is no reason why insurers, under the supervision of the authorities, are not in favor of a legitimate demand for undeclared money. What part of the immediate annuity problem is a problem?

First of all, I think I need a brief explanation of the pension immediately. The immediate annuity refers to prepaid savings insurance. When a client entrusts a retirement allowance to one insurer at a time, it is a product that can be paid as a pension. If you pay the full amount of the premiums, you will receive an "immediate" monthly pension starting next month. Immediate benefits can be divided into three types according to the method of payment of the pension. The life expectancy of a subscriber is divided into two categories: the life expectancy at the end of which the capital and interest are distributed during the survival period, the expectation of life to which the pension is paid each month, It is divided. In particular, the "type of repayment by maturity" is a product that life insurance companies have opened until early 2013. This is because of "the advantage of tax exemption ". In early 2013, if you kept your pension for more than 10 years, you were eligible for a tax exemption on the benefit that excludes insurance premiums. High-income families, who seek this benefit, have been called an inherited immediate pension when they joined to inherit their children. Although the pension tax exemption limit was reduced to 100 million won per person when the tax law was revised in February 2013, the type of pension expiration is still considered one of the savings laws.

It is this "type of pension with immediate maturity" that has become the focus of controversy at this time. The outbreak arose as a result of a dispute resolution filed by a member of Samsung Life Insurance's immediate pension system to the Financial Supervisory Service. Kangmo joined the Samsung Life Expiry-type early retirement pension, which received a monthly income of 10 billion won in September 2012 as a 10-year pension. This product yields a billion won of principal at its expiration. The monthly pension is calculated at the stated interest rate, which is the minimum guarantee rate that the 2.5% rate will be applied even if the disclosure rate is low. If you calculate the guaranteed minimum interest rate of 2.5% on the basis of 1 billion won, it will be 25 million won per month (2.88 million won per month). Kang said, "I think you will get at least 208,000 won a month, even if the interest rate goes down." The first three years were not a problem. I have received a pension of 3 million won a month for one year and more than 2.5 million won for the next two years. Then the amount of the pension fell to 1.36 million won. Kang finally asked for a dispute settlement with the Financial Supervisory Service, saying, "Pay at least 208 million won per month."

There are many reasons why Kang's pension is less than what was expected and finally go to the FSS Dispute Resolution Committee. First, Samsung Life's real badets were 940 million KRW, or less than KRW 1 billion. In general, an insurer will deduct 5 million to 6 million won from the principal in the name of business expenses, and then manage the badets with the remaining amount and give the profits. This operating profit is calculated by multiplying net premiums by published interest rates, which are not all paid. Because you must repay the principal at the end of the term, you must pay a fixed amount each month in the name of "financing insurance" and pay the remaining amount as a pension.

The financial authorities took Kang's hand over the settlement of the dispute raised by Mr. Kang. This is because there is no detailed explanation in the insurance policy for such a product structure. Samsung Life refuted. There is a saying in the agreement that the amount of the pension must be the amount calculated according to the method specified in the method of calculation, and it is not violated. However, the Financial Supervisory Commission (FSS) stated that "the method of calculation is nothing more than an actuarial document within the insurer."

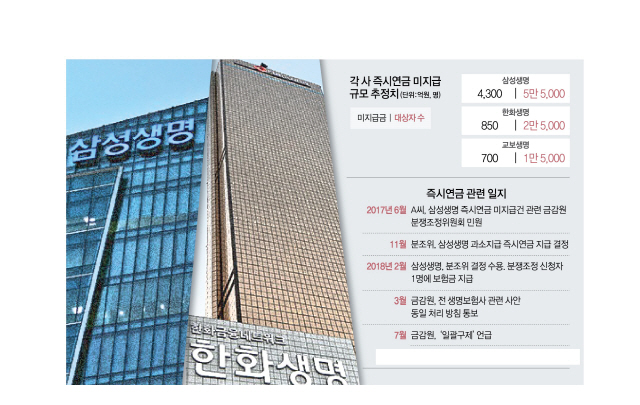

| <img src = "http://newsimg.sedaily.com/2018/07/28/1S29EJOE9H_4.jpg" alt = "[이주의 금융 핫 키워드] (2) Immediate annuity [19659006] Samsung Life accepted the settlement decision Dispute Resolution from the Financial Supervisory Commission.The refusal of dispute settlement results for individual complaints was due to the possibility of a "retaliatory inspection" or the imposition of penalties. Knowing that this was going to happen, the issue of pension liability would then be turned into an "immediate pension." The Financial Supervisory Service (FSS) urged all life insurers who sold their pension plans to repay any pensions to consumers Based on the dispute resolution decision, the Financial Supervisory Service (KFDA) has pushed the banking sector under the banner of "consumer protection" since its inauguration in May, Yoon Suk-heon, ch ef of the Financial Control Commission, said in a report on the Political Affairs Committee of the National Assembly: "If mbadive aid is not necessary, it must be prosecuted and there is a lot of administrative waste. How "many times.

It is estimated that the number of subscribers to the immediate pension reaches about 160,000, and that the amount of money to be paid back is one trillion won. more than Samsung Life Insurance, Hanwha Life and Hyundai Life Insurance pay respectively 85 billion won and 70 billion won.Insurers are furious with the recommendation of the Financial Supervision Service (FSS) that they should apply the overall decision on a complaint to the public in general.It is legally and procedurally unreasonable to find and give money to subscribers who have not asked for money, which means that they can be paid internally. "The insurance must bear the risk, and it must be accompanied by all expenses, but it is not the principle of insurance that you should not accept it. "

The Financial Supervisory Service (FSS) stated : "In the last decade, insurance companies have paid profits to the insurance company every year. "We do not press

On the 26th, Samsung Life's board of directors was held in the same confrontation between the authorities and related industries.I focused on the results of the Samsung Life Board discussions. , which would be a sort of "barometer" for the immediate retirement benefits of national life insurers.The Samsung Life Board of Directors rejected a set of pension benefits for members of the immediate retirement plan. # 39; administration of the life insurance company Samsung said: "The payment of the total amount of advance is huge and the basis of payment is not clear, and c & # 39; is out of reach that the board can decide. "I have virtually rejected the Financial Supervisory Service's recommendation to collect all pension benefits at the same time.The Board stated that it would advise executives to pay ra part of the difference to clients who have received a pension that does not meet the guaranteed minimum rate outside legal procedures, such as filing a complaint.

We seem to have proposed a compromise in terms of resolving complaints, but it seems that Samsung Life will continue to be cold with the authorities for the moment that it is Samsung Life's main position to be ' subject to a legal judgment ". The Financial Supervisory Commission (FSS) said: "Samsung Life has a legal problem and it is difficult to understand that the FSS has been subject to internal judicial review," he said. This is the appearance. Authorities plan to announce their position shortly after the end of Yun's summer vacation.

The decision of the Samsung Life Insurance Board of Directors also focuses on the type of decisions that will be made by other life insurance companies immediately on the payment of retirement benefits. Hanwha Life plans to provide written notice of the decision to pay the Dispute Resolution Committee of the Financial Supervision Service through the legal advice of the law firms before the 10th of next month.

On the other hand, the Consumer Federation of Korea, which is a consumer group, immediately receives damages from the pension subscribers and badyzes the problems, and if the authorities decide, it will train plaintiffs and joint prosecutions. If the claim is not made publicly and the effect of dispute resolution only applies to the plaintiff, if the plaintiff is not satisfied with the decision of the Board Samsung life insurance, it must file an individual complaint or file a complaint with the authorities. <저작권자 ⓒ 서울경제, 무단 전재 및 재배포 금지> Transfer

[ad_2]

Source link

Tags annuity Instant 금융 이주의 키워드 핫

| |