[ad_1]

The Fed could instantly claim victory and pocket congratulations.

For the first time in its history, the Fed is formally and vocally considering using monetary policy to increase inflation, or at least inflation expectations. On Friday, Chicago Fed President Charles Evans embodies this message in the minds of consumers and recalcitrant workers, whose fruits of their labor are devoured by inflation:

"Because inflation expectations seem to be lower than our target of 2% and that's stubborn … it tells me that our current policy framework is restrictive," he said. told the press. He sees two rate cuts this year, 25 basis points each, not because the economy needs it, but to make it clear to consumers and workers that their hard-earned dollars are not losing their power fast enough. of purchase and that they should change their habits. attitude and expect with gratitude more inflation.

But the problem is not that there is not enough consumer price inflation. There are plenty. Everyone has their stories. Inflation is different for everyone. When your rent increases by 10% and 50% of what you earn is rented, your health insurance premium increases by 30% and 20% of what you earn is paid to health insurance, no matter what your point of view. you have a shit of inflation on your hands.

And so that you can cope with this increase in your cost of living, there is a wage inflation of 3%, hahahahaha ….

Other people do not experience this type of massive inflationary pressure. They can live in places where rents are flat. Homeowners – more than 60% of households – have little inflation on the housing front unless they move. The electronics, furniture, appliances, clothes, shoes and many other things have become cheaper over the years if you know how to use the internet. So everything depends. And all this is averaged in the United States, all over the United States, and these data are summarized in various indices of consumer price inflation.

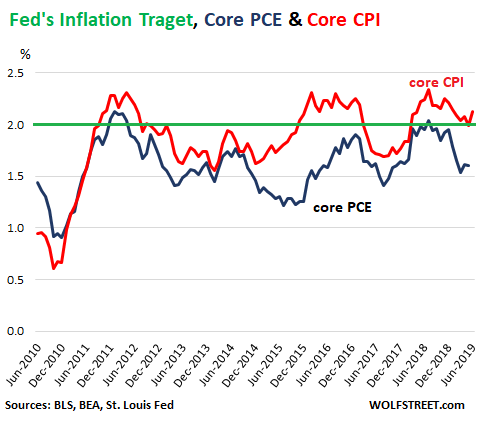

The PCE is the consumer price index that the Fed uses as a benchmark for "price stability" at 2%. This index generally shows the lower inflation of the main indices. And the Fed focuses on the PCE index without food or energy because these two categories are very volatile; food and fuel prices can go up and down.

The Fed's target is "symmetrical", as it constantly says, which means that inflation can be slightly above or below the target without triggering a monetary reaction.

Then there is the consumer price index, or CPI. It also contains a "main" version without food or energy, which makes it much less volatile. The CPI is generally higher than the PCE index.

The CPI continues to complain: it does not reflect the full weight of the rising cost of living for consumers and workers. As mentioned above, inflation is experienced differently by everyone and no one will be satisfied with the national average, but that's what we have.

Nevertheless, the core CPI is a little less unrealistic than the basic CPE. The chart shows the main PCE (blue) and CPI (red), as well as the Fed's objective (green). Note that the red line (core CPI) has been slightly above or below the Fed's target in a relatively "symmetrical" way since the Great Recession. If the Fed chooses as a target core CPI, its mission of "2% price stability" is fulfilled and would have been accomplished for years. She can garner global congratulations for having "accomplished" her mission:

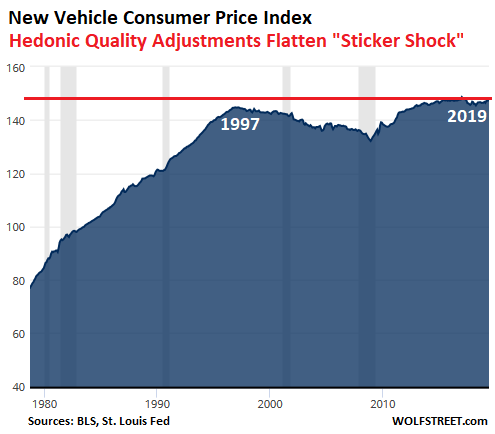

To further improve the Fed's success rate, after changing its basic CPI benchmark, it could have prevented the Bureau of Labor Statistics (BLS), which combines the CPI, from being less aggressive with hedonic quality adjustments ".

"Hedonic quality adjustments" make sense conceptually. For example, with cars. They are much better today in many ways than in 1980. Performance, comfort, safety (multiple airbags, side impact protection bars, deformation zones, anti-lock brakes, traction control, brake systems). warning, etc.), electronic dreaming in the 1980s, reversing cameras, suspension systems, emission control systems, materials, durability, etc. All of this costs money to develop and build.

So, if new cars are improving year by year, this extra cost, added to the price of the car, is not in principle inflation, because you get a better product and you pay more. Your cost of living is increasing, but you are probably safer and more comfortable and enjoy a better quality of life.

This is a key element of inflation: if your cost of living rises because you buy higher quality products, the share attributed to the cost of that quality is not inflation: yes, life becomes more expensive, but the situation is probably improving and this part is not inflation. Inflation is when the same thing with the same qualities becomes more expensive.

Thus, price increases based on product improvements are adjusted from the inflation index. According to the BLS, these "hedonic quality adjustments" for new vehicles are based on these factors: reliability, durability, safety, fuel economy, handling, speed, acceleration / deceleration, load capacity, comfort or convenience, and adding or removal of material.

This gives us a situation where new vehicle prices show virtually no inflation since 1997, when real transaction prices jumped:

Conceptually, I get these quality adjustments. But they apply to many elements, such as consumer electronics and the big cost, the cost of housing (rent and "equivalent rent of the owner's main home", which means an apartment, a house or a condo more agreable). And even slightly aggressive Quality adjustments, spread across all items in the basket, have a significant impact on the particular world of the Fed's judgment, where people work at one or two tenths of a percentage point – for example, a rate of 40 percent. annual inflation of 1.8% (below the target set). = Fed failed) versus 2.0% (on target = the Fed succeeded).

But these quality adjustments are aggressive – and probably overly aggressive – where real inflation is underestimated by a relatively small amount that makes a huge difference in terms of monetary policy where a five-tenths change in percentage can cause the Fed to do hyperventilation, especially on the lower pulling side.

The Fed must therefore first move from the ECP measure to the core CPI, which would solve just about all of its current problem of "low inflation" in one fell swoop.

And then, once the change is made, the Fed must have the data points so that the BLS is less aggressive in its quality adjustments. Just a little here and there. And the core CPI, even with current prices, would be excessively higher than the Fed's target and "low inflation" would be defeated.

The Fed could claim the victory on the "low inflation" front, win the victory and build its flawless credibility on the fact that it will always defeat "low inflation". She could then go back to the rhetoric of how she contain inflation, and how this push of inflation was just "transient", or something else.

Oh, it's good here. But we are a little embarrassed to call him. Lily… With all this impression of money, where is the huge inflation?

Do you like to read WOLF STREET and want to support it? Using ad blockers – I fully understand why – but you want to support the site? You can give "beer money". I like it a lot. Click on the beer mug to find out how:

Would you like to be informed by email of the publication of a new article by WOLF STREET? Register here.

[ad_2]

Source link